- The Borrow Smart Chronicles

- Posts

- 2026 - Setting Up to be 'Amazing'

2026 - Setting Up to be 'Amazing'

If you are flexible, and focused, the wind should be at your back!

Todd Ballenger

January 12, 2026

"Step into the new year like a quiet investor in yourself—patient, optimistic, and willing to compound small, courageous choices into something extraordinary.”"

IMPORTANT NOTE:

In 2026, I will send the Newsletter on Mondays. It gives me the weekend to work on a topic of interest. I will release my favorite charts of the week on Friday, so now you’ll hear from me twice a week. I hope that’s okay…

Please let me know what you’d like me to explore further. You can email me at [email protected].

a BORROW SMART CONCEPT

Why 2026 Looks Good to Me?

Fewer Loan Officers. More Production.

That’s the Shift.

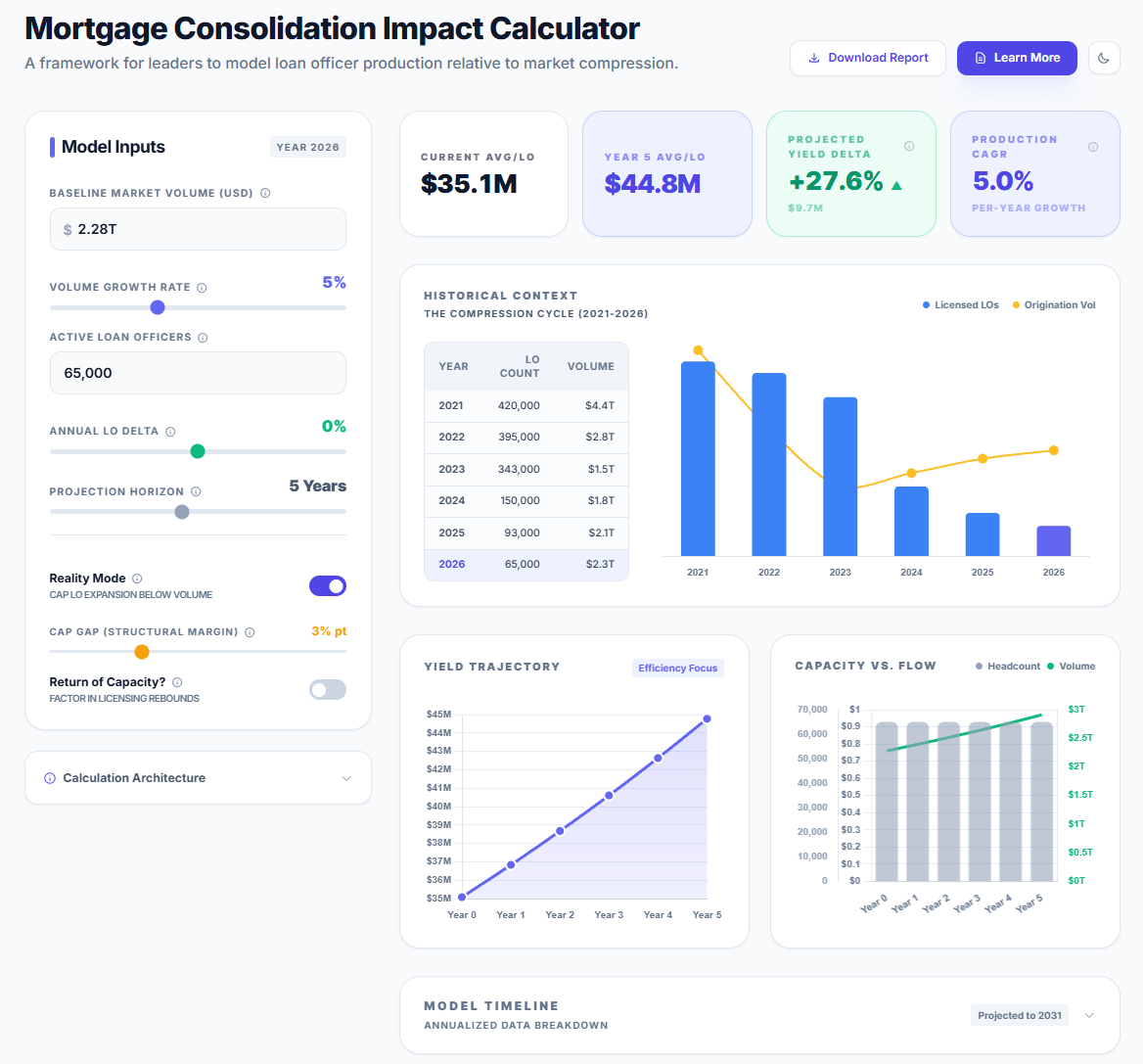

This chart tells a story most people miss at first glance. Every January, we publish a presentation to our partners on the critical headwind. This year, I’m sharing it with you as a live dashboard.

From 2021 to 2026, the number of licensed residential loan officers collapses — from roughly 420,000 to ~65,000. At the same time, total mortgage origination volume stabilizes and begins to recover, moving from ~$1.5T back toward ~$2.3T.

That means one thing:

Average production per loan officer is heading UP (meaningfully).

What’s actually happening

In 2021, $4.44T spread across ~420K LOs = ~$10.6M per LO

By 2026, ~$2.28T spread across ~65K LOs = ~$35M per LO

That’s more than a 3× increase in per-officer production in just five years.

This isn’t a temporary anomaly. It’s a structural shift:

Fewer, more professional operators

Better tech leverage

Higher client concentration

Less “tourist” capacity in the industry

What happens next if volume only grows 5% per year?

Here’s the non-obvious insight.

Even if total mortgage volume only grows at 5% annually, average production keeps rising sharply — because capacity doesn’t come back the way people expect.

Assume:

Loan officer count stays flat (or grows very slowly)

Volume grows at just 5% per year

Simple math (directionally correct):

Year 0: $2.28T ÷ 65K ≈ $35M per LO

Year 5: $2.28T × 1.28 ≈ $2.9T total volume

$2.9T ÷ 65K ≈ $44–45M per LO

That’s another 25–30% increase in per-officer production — without a boom, without refis, and without rate miracles.

The takeaway most people are missing…

This is not a “when rates drop” story.

This is a power-law industry reset:

The middle hollowed out

The top got stronger

Average productivity permanently stepped up

In the next cycle, success won’t come from doing more loans —

it will come from controlling better decisions, better advice, and better leverage per client.

The era of the $10–15M LO is over.

The era of the $40–50M LO is just getting started.

Key Borrow Smart Concept - It’s a Marathon, not a Race

Everything compounds… out live out last.

Click the image to view an interact - this is updated every January

Was this email forwarded to you? Sign up here.