- The Borrow Smart Chronicles

- Posts

- Concentrate to get Wealthy

“Money is a terrible master but an excellent servant.”

The Wealth Ladder, as outlined by Nick Maggiulli, divides wealth into six distinct levels, primarily based on logarithmic net worth ranges (each level is roughly 10 times larger than the one before it). This framework is designed to help individuals understand how their financial strategy should evolve as their wealth grows, emphasizing that different levels unlock different financial freedoms and require different approaches to managing money. The one common denominator I got from reading his book - continuous learning is THE differentiator to move from one level to the next!

Here is a clear outline of each wealth level:

Level One:

Net Worth: Less than $10,000.

Household Distribution: Approximately 20% of U.S. households are in this level.

Focus: While not explicitly detailed as a focus in the provided text, the discussion implies that individuals in this early stage are likely focused on foundational income generation and expense management, as investments have minimal impact at this point.

Level Two:

Net Worth: $10,000 to $100,000.

Household Distribution: Roughly 20% of U.S. households are in this level.

Spending Freedom: By the end of Level Two, individuals unlock "grocery freedom," meaning they can buy what they want at the grocery store without significant impact.

Key Strategy: The primary focus for advancing from Level Two is education and skill-building that can increase income. Investment returns are relatively small at this stage, so long-term income growth is the crucial "wedge" for building wealth. It's about learning something valuable in the marketplace that can generate income.

Mobility: There are two types of people in Level Two: those who just need time to advance due to good education and income, and those who need to change their strategy because time alone is not enough.

Level Three:

Net Worth: $100,000 to $1 million.

Household Distribution: This is the largest group, encompassing about 40% of U.S. households, often considered "middle-class America".

Spending Freedom: By the end of Level Three, individuals achieve "restaurant freedom," able to buy most entrees at restaurants without concern, except for the most expensive wine bottles. This is supported by the "0.01% rule," where a million-dollar net worth generates about $100 per day (on an annualized basis of 3.7%), allowing for occasional splurges without worry.

Key Strategy: The primary strategy for Level Three is "just keep buying" – the continual purchase of a diverse set of income-producing assets. At this level, compounding begins to make a significant difference, and the investment portfolio starts to compete with the individual's income in terms of wealth generation.

Challenges: Some people in Level Three struggle to advance to Level Four because they spend almost as much money as those who successfully make it to Level Four, often overpaying for housing due to "keeping up with the Joneses".

Level Four:

Net Worth: $1 million to $10 million.

Household Distribution: Approximately 18% of U.S. households are in this level.

Spending Freedom: Level Four brings "travel freedom," allowing individuals to do almost anything except fly private. This includes staying at very friendly hotels and upgrading to first class.

Key Strategy: The focus shifts significantly to diversification, taxes, and risk management. The impact of financial decisions is 10 times larger compared to lower levels. While it's still about continually purchasing diverse income-producing assets, there's a greater need to protect wealth. Counterintuitively, individuals may need to take less risk as they build more wealth to avoid significant setbacks that their income might not easily recover.

Mobility: This is considered the "no man's land of wealth," as it is the hardest level to get out of. Historically, about 64% of households in Level Four remain in Level Four after 20 years. To ascend to Level Five or Six from here, it typically requires concentrated positions or direct business ownership.

Level Five:

Net Worth: $10 million to $100 million.

Household Distribution: The top 2% of U.S. households collectively comprise Level Five and Six.

Key Strategy: To enter Level Five or Six, concentrated positions and direct business ownership become incredibly important. The adage "concentrate to get rich, diversify to stay rich" applies, meaning aggressive, focused strategies are often necessary to reach these tiers.

Other Considerations: At this level, the impact of taxes becomes even more pronounced, making professional tax advice very useful, as mistakes are much larger. People at this level are also more likely to own and enjoy fixed-income assets.

Downsides: Maggiulli believes that at a certain point, more wealth can "ruin your life" by damaging relationships and creating paranoia about being used for money, which he associates with the experiences of individuals at Level Five and Six.

Level Six:

Net Worth: $100 million plus.

Household Distribution: As with Level Five, the top 2% of U.S. households collectively comprise Levels Five and Six.

Key Strategy: Similar to Level Five, entry often requires highly concentrated bets and business ownership.

Challenges: Maintaining wealth across generations (the "shirt sleeves to shirt sleeves in three generations" phenomenon) is a significant challenge due to the doubling of family members each generation, leading to wealth dilution, and the natural decline of businesses over long periods.

Ego: At the higher levels (Level Five and Six), ego can become the "most expensive thing some people own," preventing them from diversifying or making strategic choices to protect their wealth because they believe adverse outcomes "will never happen to me". house

a BORROW SMART CONCEPT

Why Call On Financial Advisors?

“Formal education will make you a living; self-education will make you a fortune.” – Jim Rohn

When financial stress starts—like rising expenses or shrinking savings—is exactly the time to act. Waiting until after you lose your job or miss payments limits your options. Liquidity is the umbrella that is taken away when it starts raining.

Smart borrowers move early, while they still have income and credit, to consolidate high-interest debt into lower-cost, more flexible financing. This preserves liquidity, keeps cash flowing, and gives you control—not crisis.

Access to credit is easiest when you don’t urgently need it. Waiting can turn a manageable situation into a financial emergency. Talk to a Liability Advisor as part of your annual planning process.

Keep me motivated! Share this Link with a friend! I want referrals :-)

“Wealth consists not in having great possessions,

but in having few wants.” – Epictetus

LIABILITIES

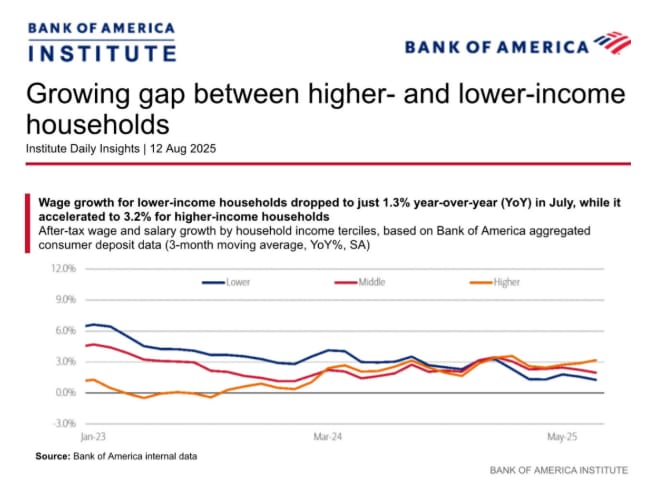

What’s Happening?

expectations for rate cuts vary from .25 to .50bps

in the past, lower rates didn’t often times lower rates… last time rates were lowered long term rates actually increased…

we are seeing trends of people tightening their belts

this home equity should be a solution, but you must be able to access it

a HELOC can be a huge financial planning tool

see my prior post - here: https://borrowsmart.beehiiv.com/p/the-art-of-asking-for

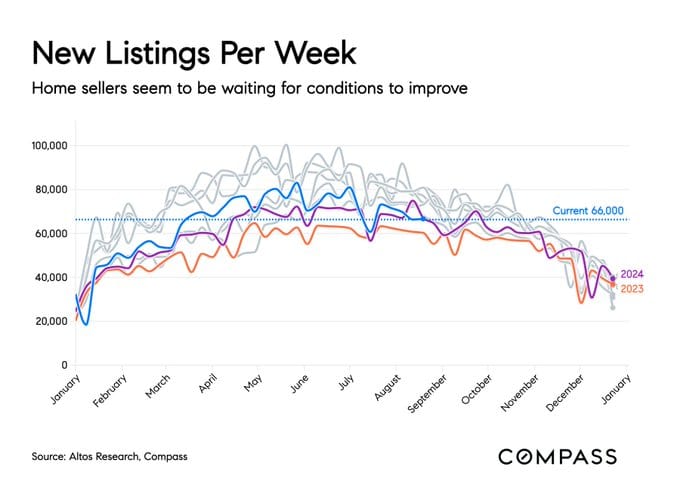

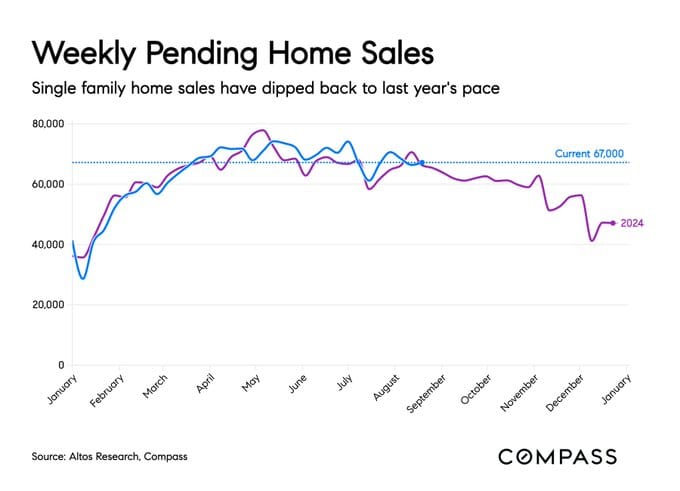

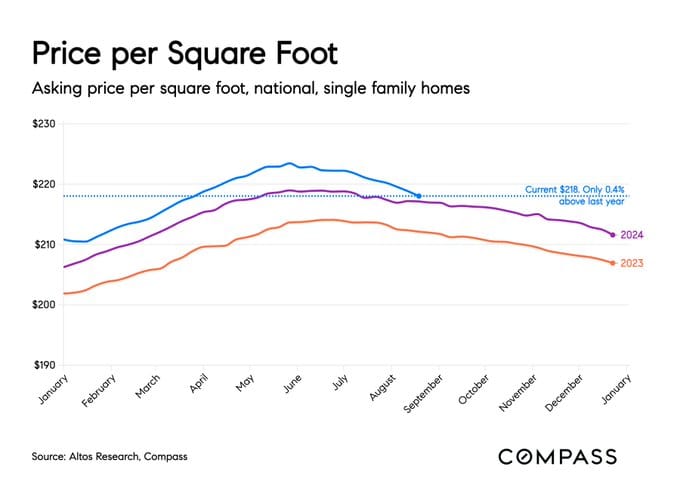

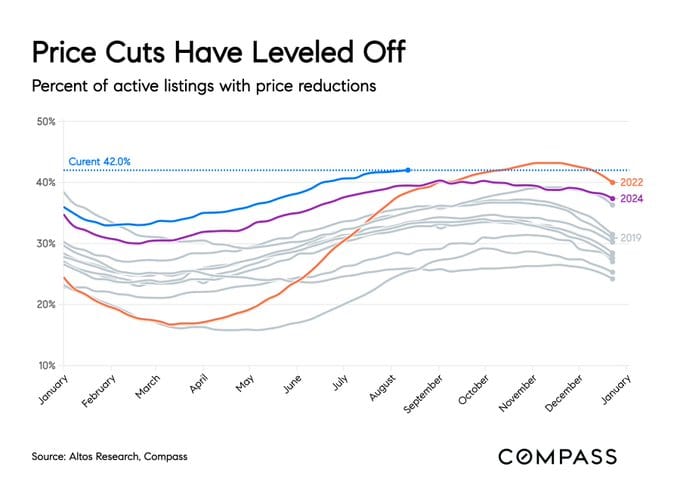

REAL ESTATE

What’s Happening?

also, did you sell FICO when they announced VANTAGE scores would be accepted? Learn how to use your advantage… did you buy RKT and NAIL? did you sell some?

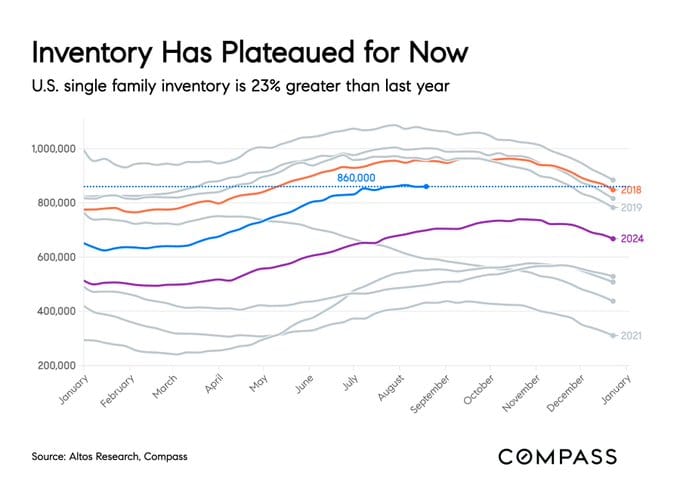

prices are flat

or declining - as we predicted they would… either rates had to come down, OR prices would…

yet, they are still crazy expensive…

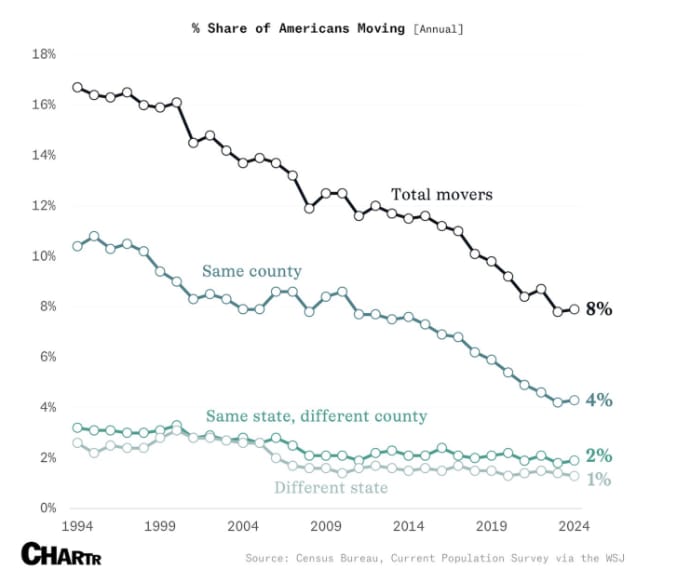

people are moving when they can to find cheaper housing

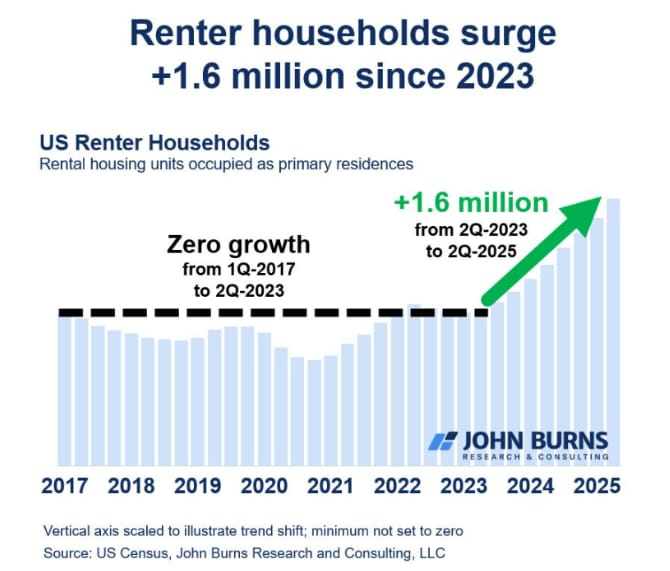

and more of those forming homes are renters for life

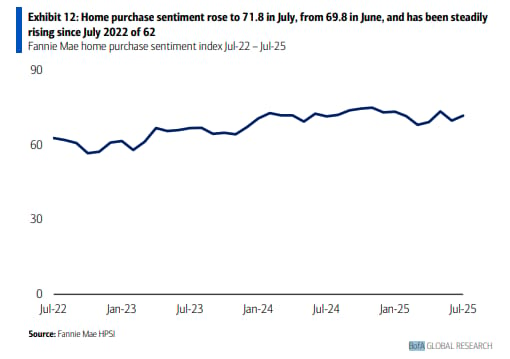

buying a home is gaining sentiment - GOOD!

and there is a huge backlog of buyers

great stuff as always from Mike Simonsen, follow him if you do not!!!

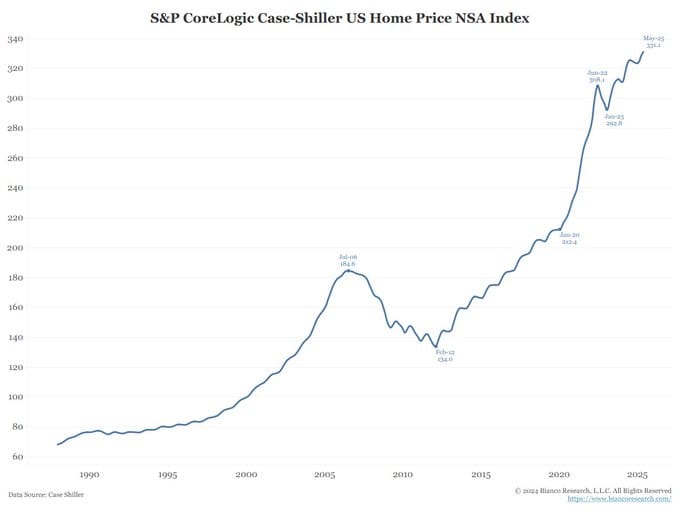

Home prices are about to turn negative again.

I illustrated the last several year of home prices to show what's under way.

— Mike Simonsen 🐉 (@mikesimonsen)

5:42 PM • Aug 16, 2025

"The best thing for being sad," replied Merlyn, beginning to puff and blow, "is to learn something. That is the only thing that never fails. You may grow old and trembling in your anatomies, you may lie awake at night listening to the disorder of your veins, you may miss your only love, you may see the world about you devastated by evil lunatics, or know your honour trampled in the sewers of baser minds.

There is only one thing for it then—to learn. Learn why the world wags and what wags it. That is the only thing which the mind can never exhaust, never alienate, never be tortured by, never fear or distrust, and never dream of regretting. Learning is the thing for you.

ASSETS

What’s Happening?

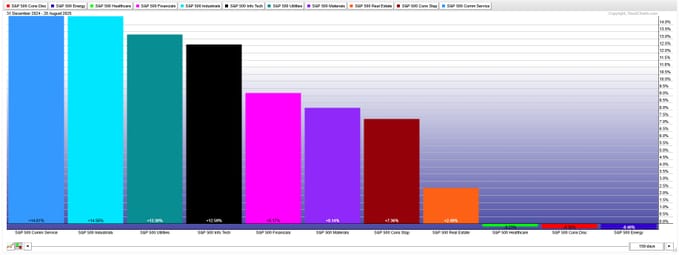

most sectors are up bigly…

and stock holding is the market for the market!

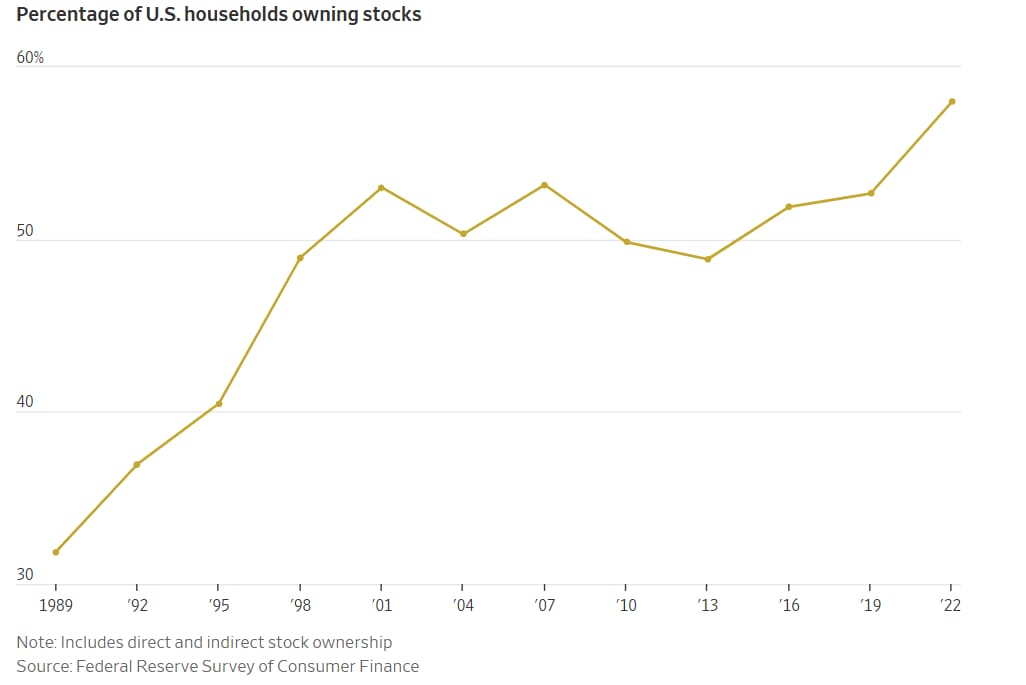

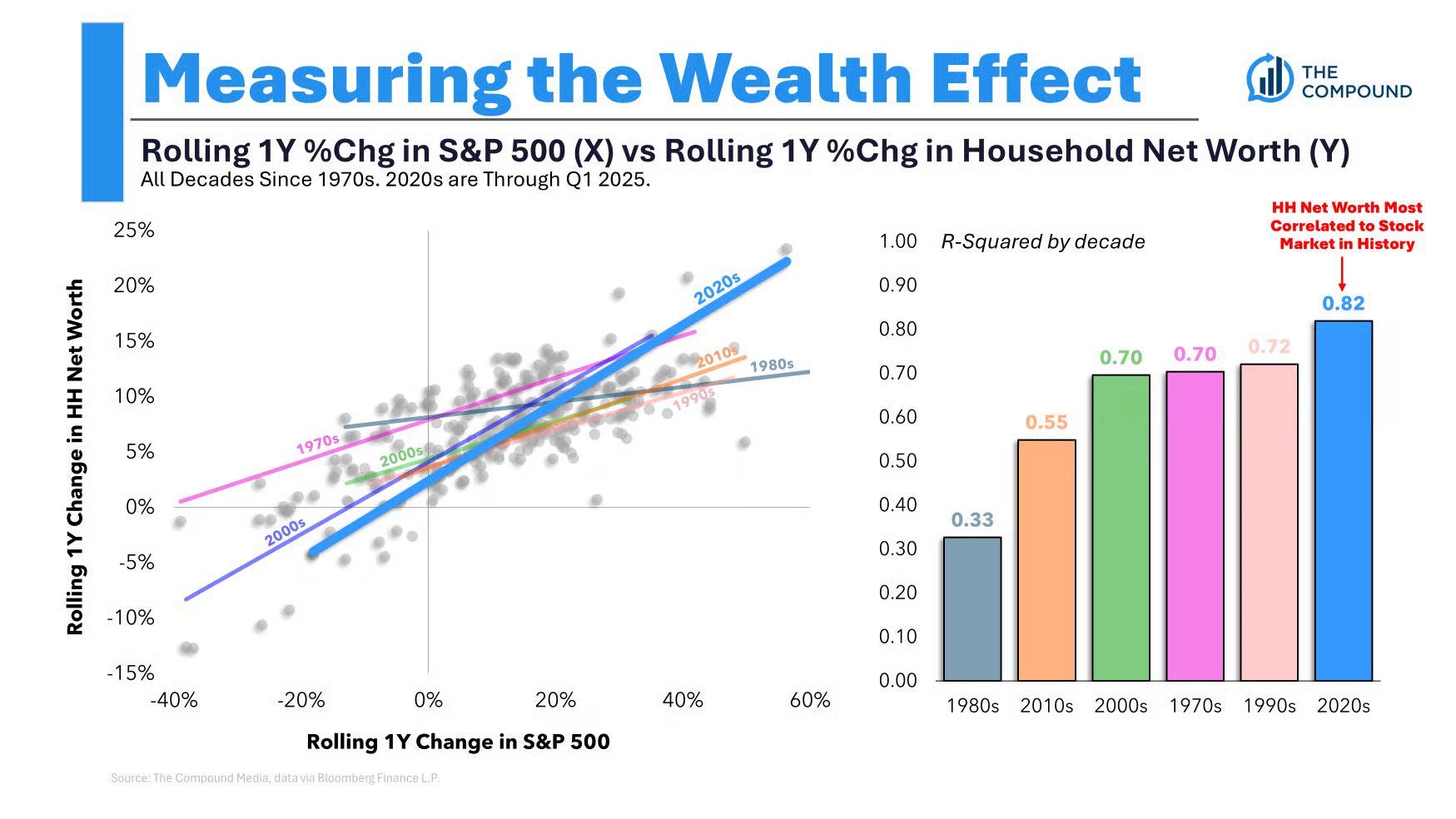

record high correlation, if the market goes down, 82% will feel it, up from 33% in the 80’s

outside the market, your investments at best are breaking even

historic $30T increase in wealth in last 20 years

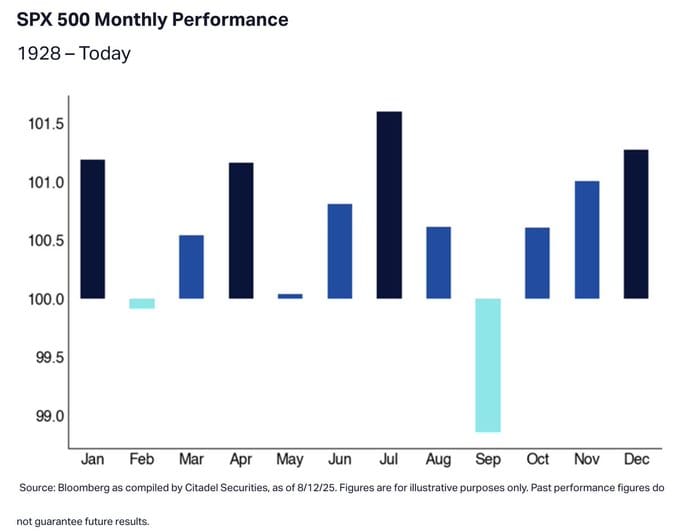

September is always precarious!

ON BEING HUMAN

What’s Worth Sharing?

Was this email forwarded to you? Sign up here.