- The Borrow Smart Chronicles

- Posts

- Debt, Inflation, Processes that Win!

Debt, Inflation, Processes that Win!

The rate of change of the rate of change is insane right now!

Todd Ballenger

December 06, 2025

Inflation is as violent as a mugger, as frightening as an armed robber and as deadly as a hit man."

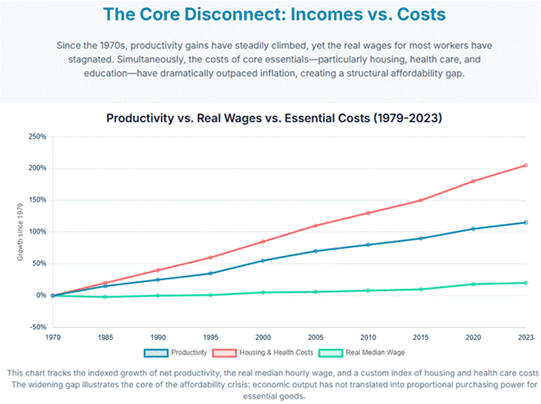

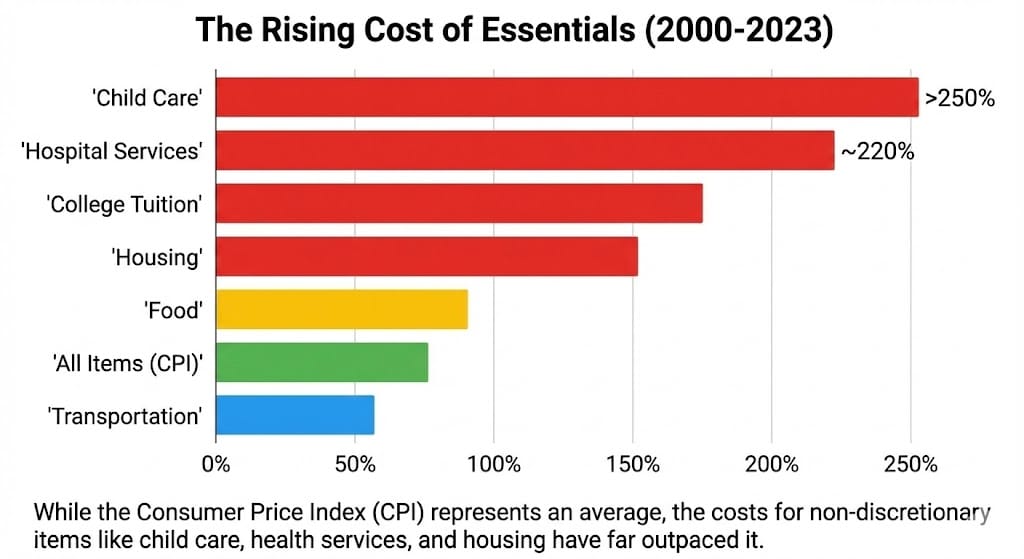

Why Adulting Feels More Expensive (Because It Is)

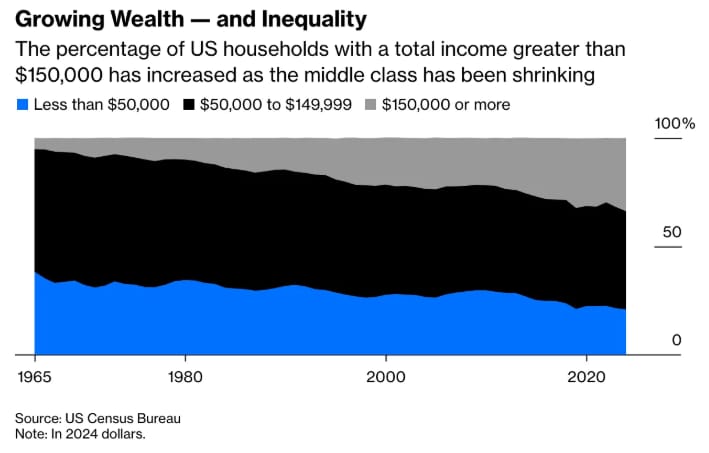

If you feel like you are working harder than ever but your paycheck isn’t going as far, you aren’t imagining things. The data backs you up.

We are living in what economists call the "Great Divergence." Since 1979, American productivity has shot up by roughly 65%, but worker pay? It only nudged up about 17%. Basically, we are getting more efficient, but our wallets aren't seeing the benefit.

The Housing Reality Check

The biggest squeeze is happening at home. The old rule of thumb was that a house cost about 3.5 times the median income. Today, the national average is 5.3 times your income (and double that if you live on the coast).

Prices have skyrocketed 408% since the mid-80s, while income only grew 241%. That math makes it tough to get ahead.

It’s Not a Bubble, It’s a Famine

Unlike 2008, when there were too many houses and shady loans, 2024 is defined by a supply famine. We are missing millions of homes that simply weren't built over the last decade. Because supply is so low, prices stay high.

The Move? Focus on Cash Flow

Waiting for prices to crash might not work in a market with no inventory. Instead of timing the market, focus on cash flow.

Borrow Smart: Structure your loans to keep monthly payments manageable.

Stay Liquid: Keep cash on hand. When essentials like food and energy cost more, liquidity prevents you from feeling fragile.

The goal isn't just buying a house; it's ensuring the cost of owning it doesn't eat your ability to build wealth elsewhere.

a BORROW SMART CONCEPT

7 Steps Applied

Here is a practical Borrow Smart Checklist designed to prioritize cash flow and liquidity. This approach shifts the focus from just "getting a loan" to actively managing your most significant liability to build wealth.

This is based on the 7-Step Solution from the Borrow Smart method.

1. Product: Match the Loan to Your Timeline

Don't pay for safety you don't need. Most people buy a 30-year fixed mortgage but move or refinance every 7-10 years.

The Check: Ask yourself, "How long will I actually keep this loan?"

The Move: You get a fixed rate for the time you are actually there, usually at a lower cost than a 30-year fixed. If you can’t go with the longest fixed period available relative to your interest rate.

2. Payment: Minimize Mandatory Obligations

The goal is to lower your required monthly outflow to maximize your discretionary cash flow.

The Check: "How do I want to repay this loan?"

The Move: Consider an interest-only or longer amortization period. This lowers your mandatory payment. You can always pay more (principal) when you have extra cash, but you aren't forced to during tight months.

3. Availability: Maximize Liquidity Before You Need It

Liquidity is your ability to convert home equity into cash. Access to this cash often disappears precisely when you need it (e.g., job loss or income drop) because banks lend based on income capacity.

The Check: "How much of my equity can I access in an emergency?"

The Move: Establish a Home Equity Line of Credit (HELOC) immediately when you buy or refinance. It costs little to set up, and you don't pay interest unless you use it. It acts as a financial safety net.

4. Amount: Calculate Your Opportunity Cost

Should you put 20% down? 50%? Pay cash? The answer lies in EPR™ (Effective Percentage Rate).

The Check: "Can I earn more on my cash than the net cost of borrowing?"

The Move: Calculate your EPR (Interest Rate minus Tax Deduction benefits). If your investment return (e.g., 6%) is higher than your EPR (e.g., 5.2%), you are mathematically better off borrowing more and keeping your cash invested.

5. Management: Review Annually

You regularly manage your assets (401 (k), stocks). You need to do the same for your liabilities.

The Check: "Is my mortgage still the most efficient tool for my current life stage?"

The Move: Conduct an annual mortgage review. Life changes (raises, new kids, retirement) should trigger a review of your debt structure to ensure it continues to support your cash flow goals.

6. Protection: Insure Your Equity

Home equity is not guaranteed; it is subject to market risk.

The Check: "What happens if the market drops or I face a lawsuit?"

The Move: Ensure you have the right insurance (Life, Disability) to cover the debt if income stops. Also, keeping equity outside the house (in a protected investment account) is often safer than trapping it inside illiquid real estate.

7. Discipline: The "Invest the Difference" Rule

This is the most critical step. If you lower your payment (Step 2) or borrow more (Step 4), you must save the difference.

The Check: "Will I actually save the extra cash flow?"

The Move: Automate your savings. If you save $400/month by choosing a smarter loan, set up an automatic transfer of that $400 into an investment account. If you spend it, the strategy fails.

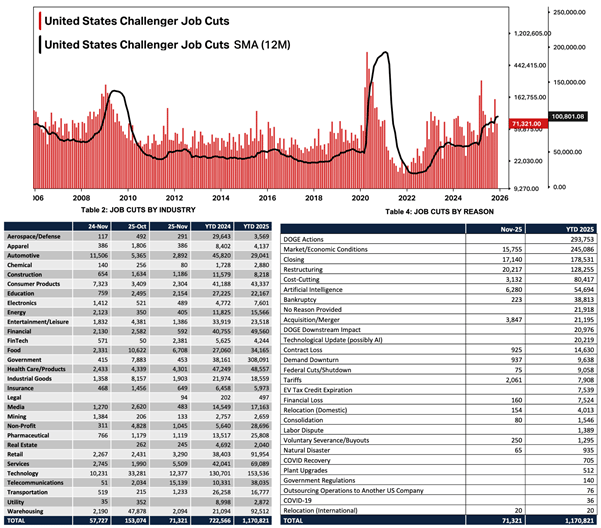

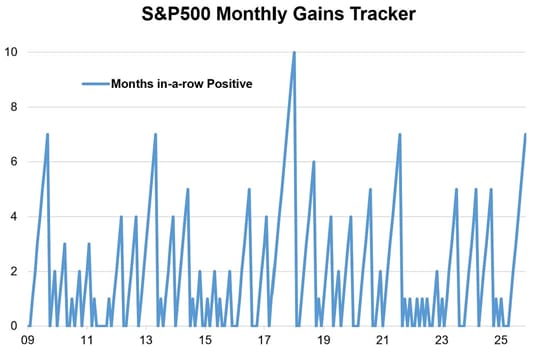

LIABILITIES

What’s Happening?

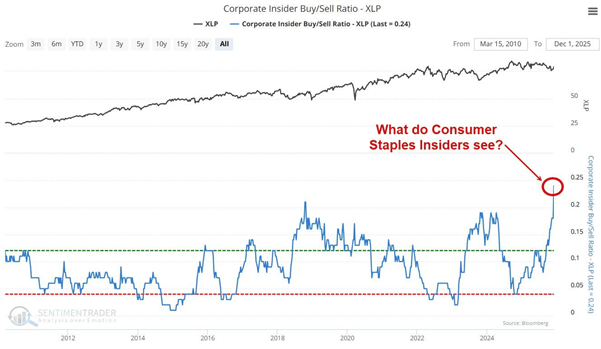

companies are doing a better job than our government

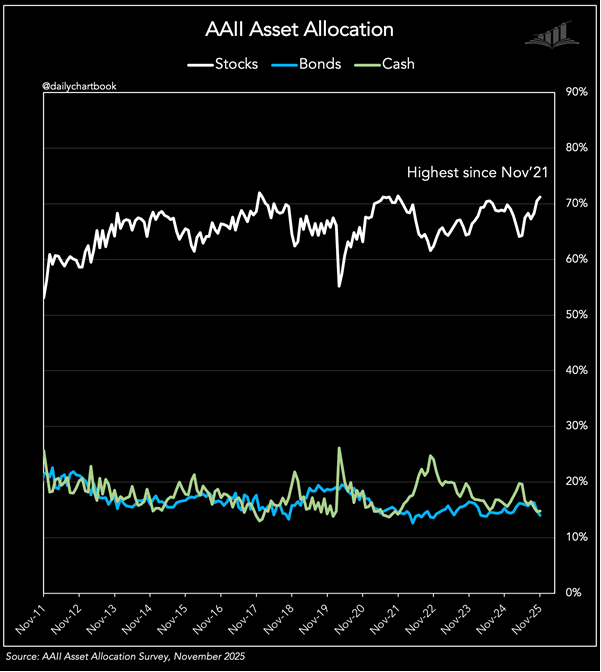

we have been higher and we have been lower, trend is turning down again

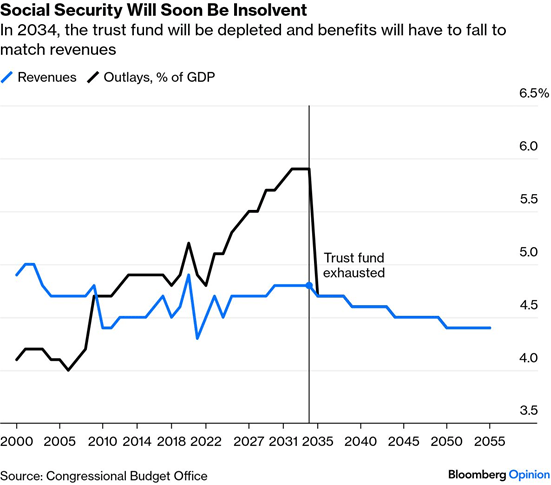

biggest risk to economy

turning up which may be ok, if employment stays strong

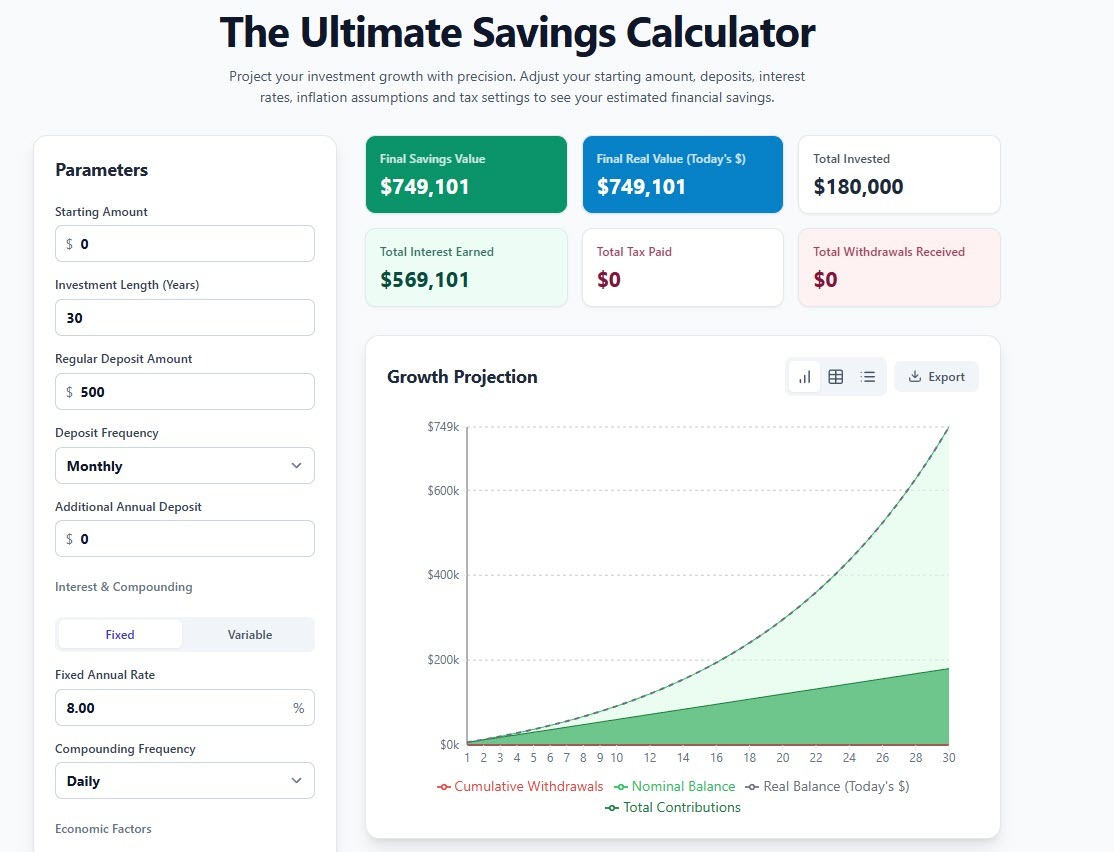

There are so many lessons and stories you can tell and simulate with a good calculator… here’s one of my favorites… share with your friends and family and make sure you understand the basics of compounding, inflation and time value of $.

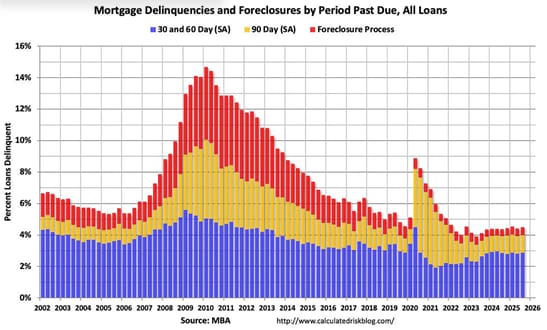

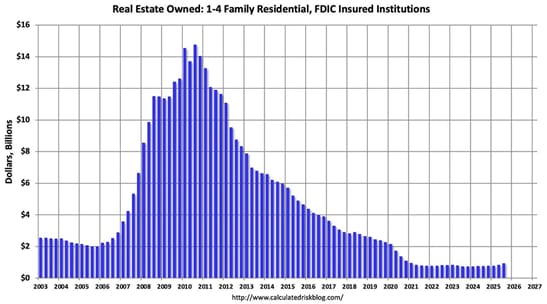

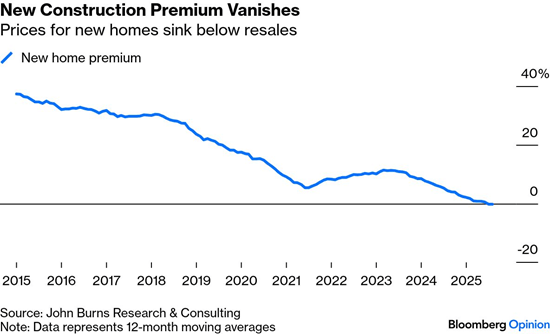

REAL ESTATE

What’s Happening?

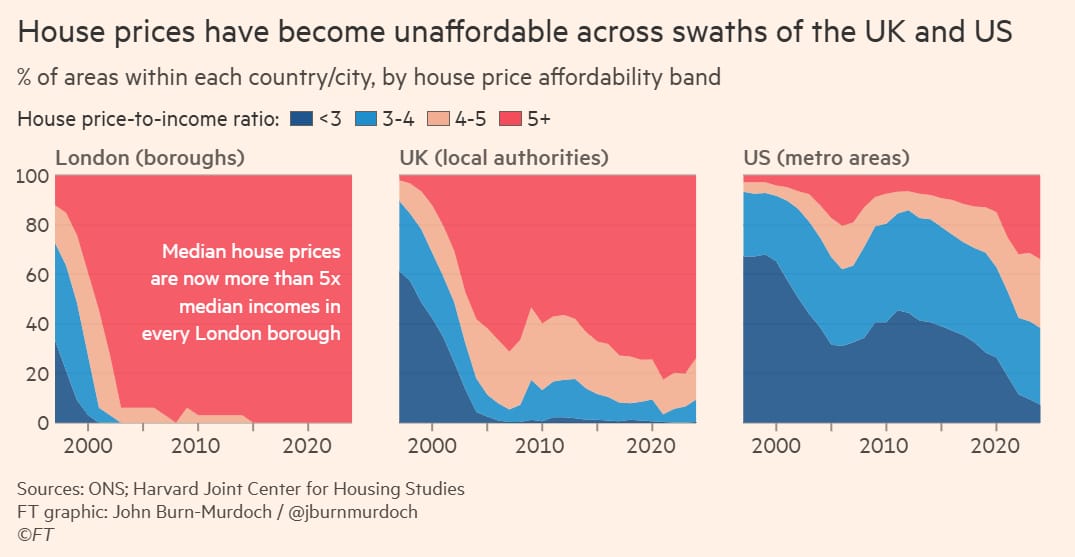

UK worse than US

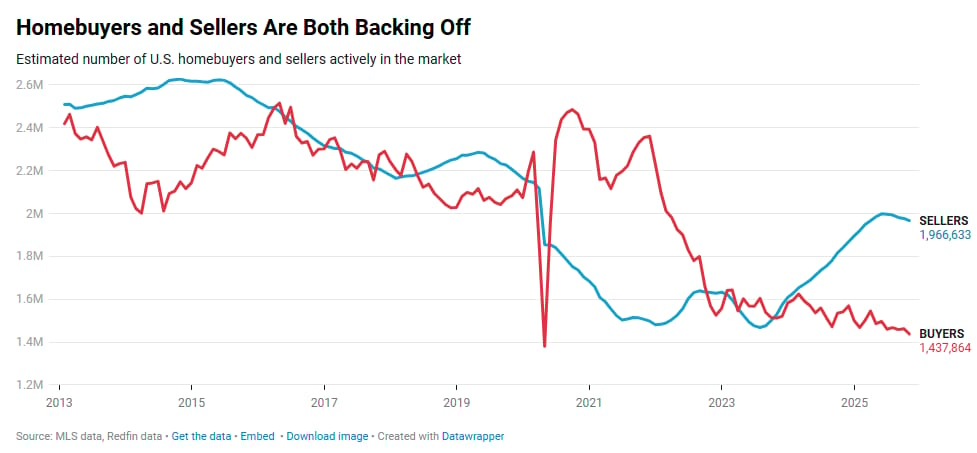

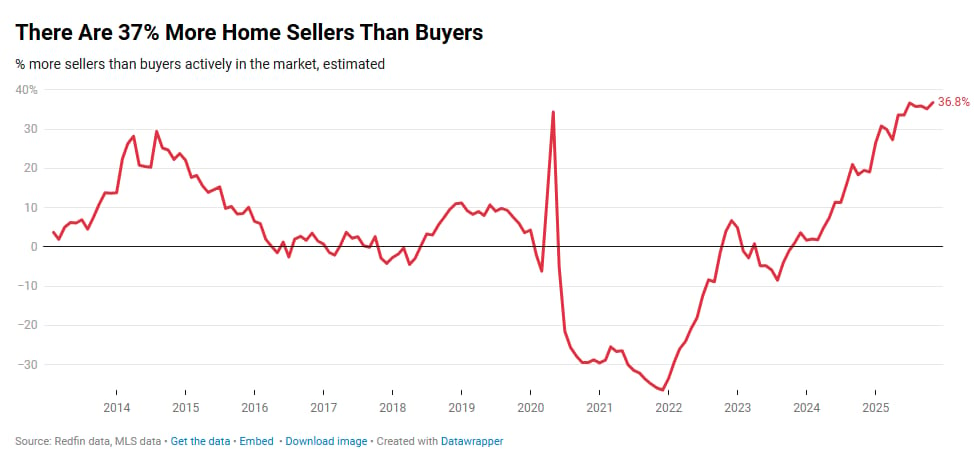

leading to more inventory

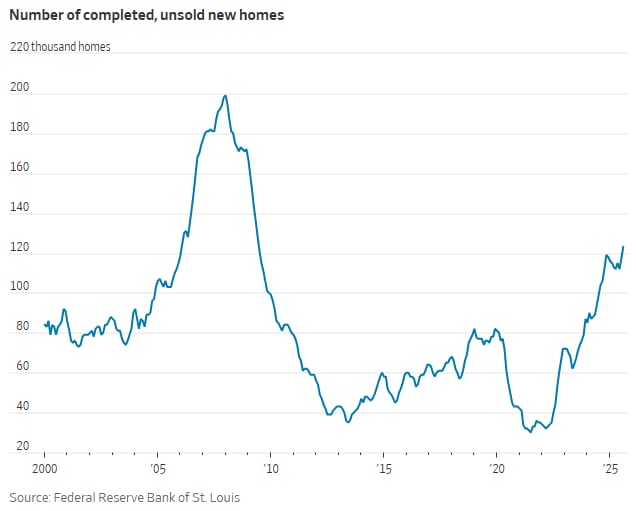

REO picking up a little as well

get a new house for less than an old one

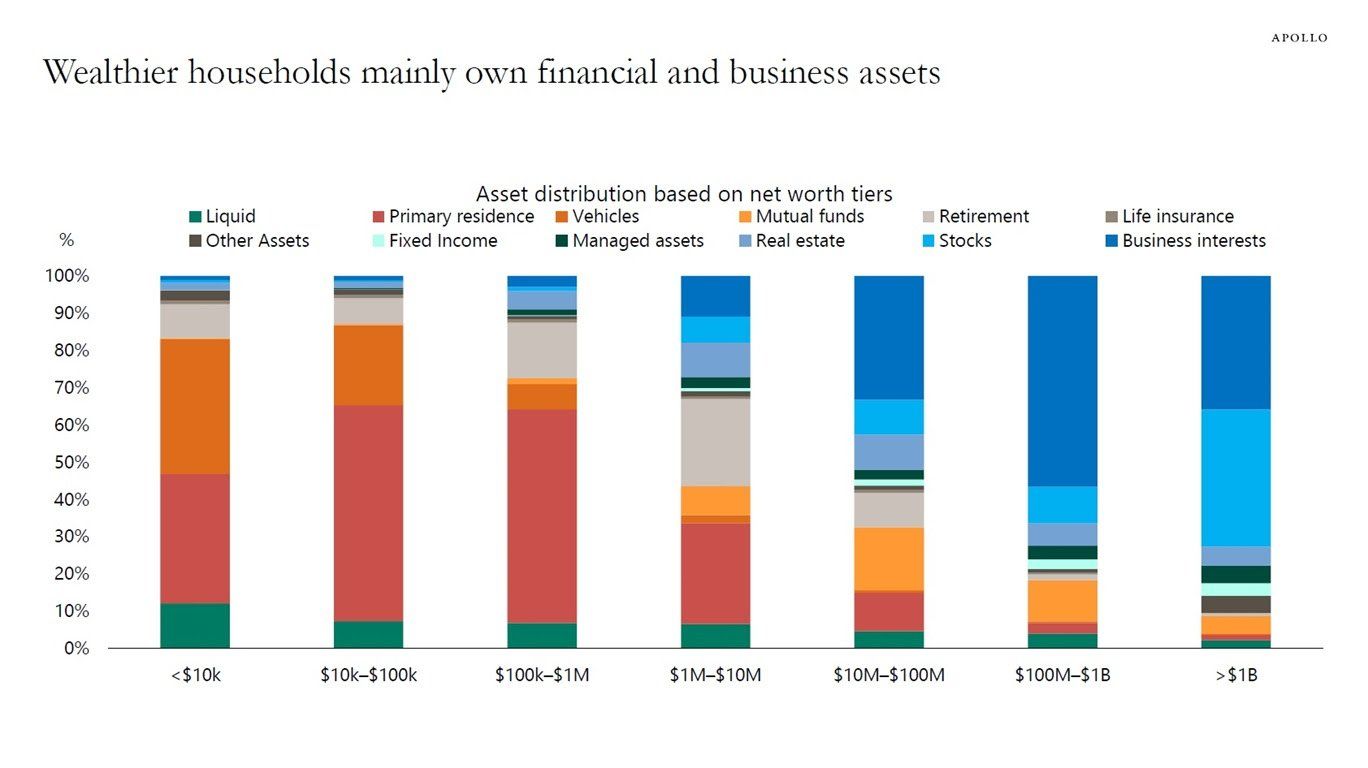

ASSETS

What’s Happening?

maybe that’s how they got wealthy?

due for a pullback?

this would piss me off

that market is frothy, but that doesn’t mean it can’t go a lot higher…

ON BEING HUMAN

What’s Worth Sharing?

DOPAMEMES

And Other Happy Moments…

Was this email forwarded to you? Sign up here.

AI

and The Future of Work…