- The Borrow Smart Chronicles

- Posts

- Financial Literacy Isn’t Optional When Money Is Your Product

Financial Literacy Isn’t Optional When Money Is Your Product

Liability Management = If You Sell Money, You’d Better Understand Money

Todd Ballenger

July 18, 2025

"If you wish to glimpse inside a human soul and get to know a person.. just watch them laugh. If they laugh well, they are good people."

© borrowsmartuniversity.com

The Overlooked Intersection: Why Smart Financial Advisors Include Liability Management

Imagine driving through your town when suddenly, you hit a major intersection under construction. What used to be three smooth lanes is now a messy snarl of detours, cones, and frustration. It’s a bottleneck. An inconvenience. A problem screaming for attention.

Yet without this attention to the problem, it might get worse. The road might collapse, or potholes might continue to eat tires. It isn’t very pleasant, but it needs attention.

Now think about this: most wealth managers are driving their clients through the intersection of assets and liabilities every day. They obsess over investments, cash flow projections, alpha, and tax efficiency. But there’s a lane that’s usually neglected — liability management.

This is not just a missed opportunity. It’s a dangerous blind spot.

Wealth is just stored money (energy) that can be release to control (energy) - you worked and saved money, that was your energy, if you hire someone or pay someone to use their resort or fly on their planes you are exchanging that stored energy - trading energy.

What’s liability management, anyway?

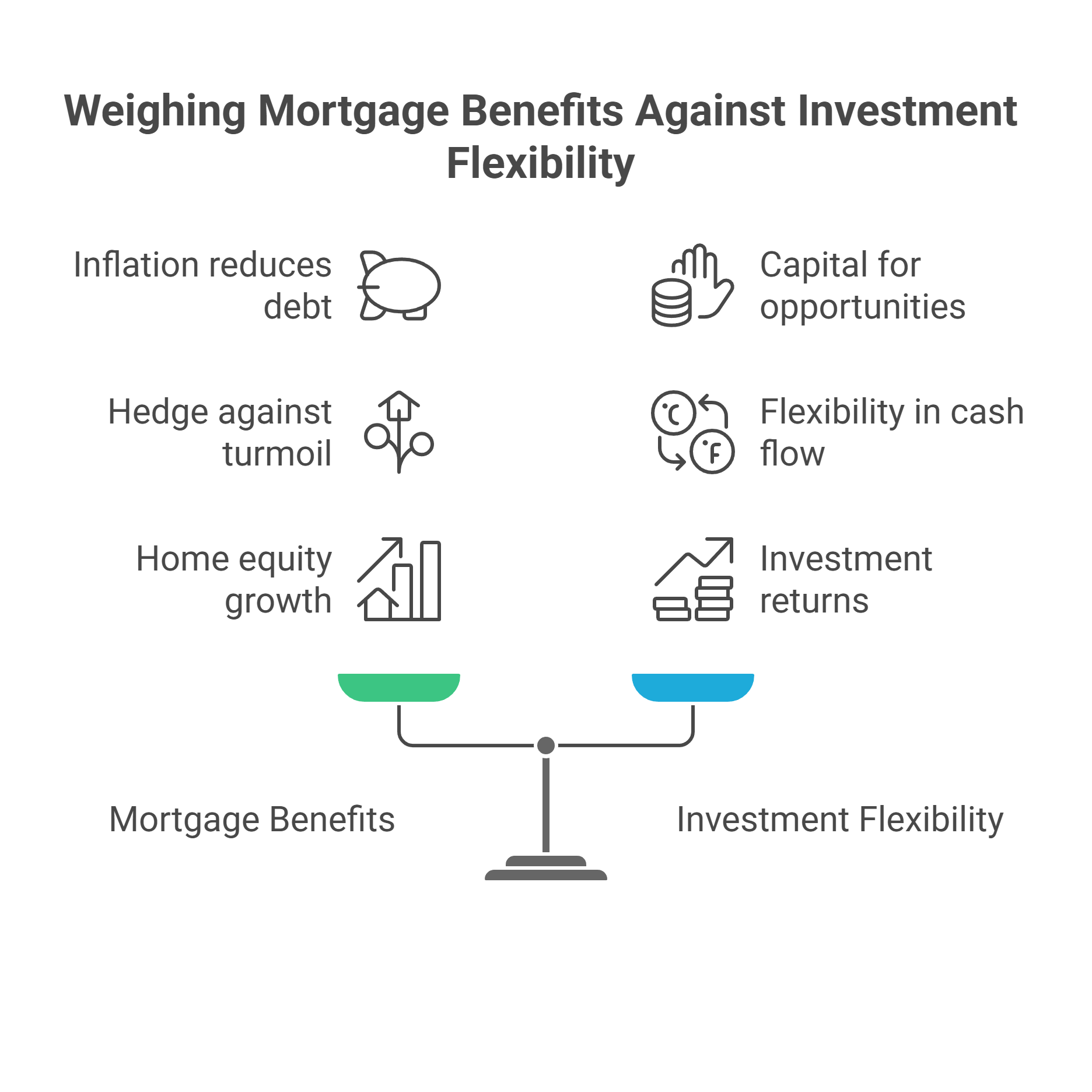

It’s not just “getting a mortgage” or “shopping rates.” Liability management is the art and science of strategically managing the other side of the balance sheet — the debts, the obligations, the leverage — in a way that protects and amplifies wealth.

Most advisors think liabilities are the dirty part of the job. They’d rather talk about the glamorous side: assets under management, growth rates, beating benchmarks. But liabilities have a secret power:

Inflation works in your favor. A smartly structured long-term mortgage means inflation eats away at your debt over time, while your real assets (like your home) often grow in value. That’s compounding from both directions.

Liquidity and optionality. Keeping capital deployed in investments — instead of sunk into home equity — means more flexibility, more cash flow, more opportunities to provide greater flexibility.

Safety in rough times. As Daniel Amerman put it, a mortgage can be a hedge against unexpected economic turmoil, acting as a buffer that protects net worth and portfolio strategy.

Return is a consideration. You’ll experience appreciation/depreciation whether you have a mortgage or not, so the real question is what you're earning on equity in the house versus being better off using that equity for other debts and opportunities. These are questions liability advisors answer daily.

KNOW THIS - High net worth clients expect more

These aren’t average borrowers. They’re entrepreneurs, executives, multi-generational families — people whose wealth is complex and interconnected. And when their liability strategy falls apart (think: poor mortgage execution, clunky loan processes), it doesn’t just cost them money. It undermines trust. It risks the entire advisor relationship.

This is why we are shifting the paradigm. When you offer scanning for better rates, simple refinancing, strategic debt optimization, annual liability reviews — and you it in the context of liability management, you are removing risk for the advisor.

What’s the takeaway?

It’s time to rethink your map.

Liability management isn’t about debt. It’s about control.

It’s about engineering a financial life where every side of the balance sheet is intentionally optimized, so clients aren’t just rich on paper — they’re resilient, prepared, and positioned to accomplish their financial goals.

Great financial advisors don’t just build roads for their clients’ assets. They upgrade the entire intersection, so the journey — and the destination — is smarter, smoother, and ultimately far wealthier.

We are finding that for every 20 advisor contacts, you should initially receive 1 high-quality closed loan per month. We recently conducted an analysis for a recent CLA in their market and found that there were 86 high-quality financial advisors within a 30-minute drive of their office…

My question for you - would you conduct 80 Zoom calls over 2 months (10 per week) with advisors if you knew it could create 4 new closings a month? What new HABITS are you forming now?

“The longer you stay on the wrong train, the more expensive it is to get home.”

a BORROW SMART CONCEPT

MONEY IS the Common Language We Speak

Why is this important?

1. You’re Selling Money—So You Must Understand It Deeply

As a lender, you’re not selling homes or houses—you’re selling money: the cost, structure, and future consequences of borrowing it. Your product is financial leverage. That makes financial literacy your most critical competitive advantage.

You’re selling interest, not square footage.

You’re influencing monthly cash flow, not just loan approval.

You’re designing long-term liability, not just completing a transaction.

If you don’t understand the economics of borrowing, the effects of inflation, amortization, tax deductions, and opportunity cost, then you’re functioning as a transaction taker, not a trusted advisor. That’s a massive liability in today’s market.

2. You’re Paid in Money—So You Must Master Its Rules

Your income as a mortgage professional is tied to your ability to explain, position, and justify why smart borrowing builds wealth. That means you must:

Know how mortgages affect net worth (not just debt-to-income ratios).

Speak confidently about leveraging equity vs. paying down principal.

Show how carrying a “big, long mortgage” can be more effective than paying it off early.

The more you understand money, the more valuable your advice, and the more sustainable your income.

3. Money Is the Common Thread in Every Part of Your Life

Unlike many professions, everything a mortgage lender touches is connected to money:

Your product is money.

Your paycheck is money.

Your equity is money.

Your client’s home ownership goals involve money.

Your success and production are measured in units of money.

In this way, financial literacy is not optional—it’s the baseline for effectiveness. Without it, you’re selling something you don’t fully understand. As the Certified Liability Advisor course points out “developing financial literacy IS the “unfair advantage” that positions you as a trusted advisor, not just a loan officer. Sermon over :-)

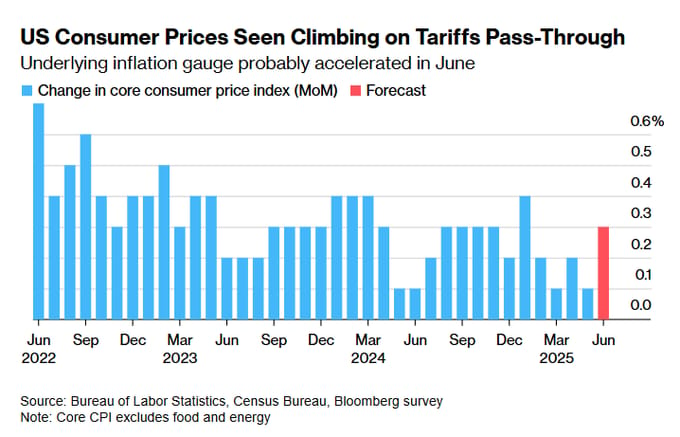

LIABILITIES

What’s Happening?

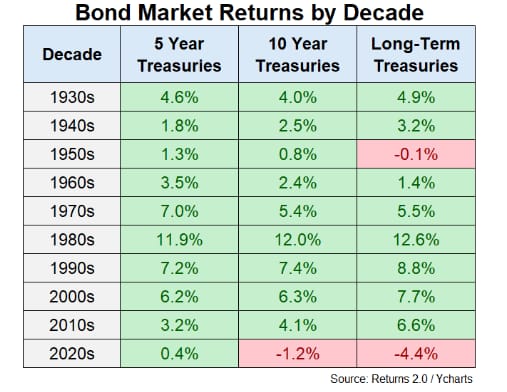

H/T Mike Zaccardi - if we were a consumer, we’d be in trouble…

remember from my book Borrow Smart Repay Smart, a bond is just a mortgage that’s been securitized, and the returns on bonds track the cost of interest

who won and who lost with the Big Beautiful Bill

"If I don't practice one day, I know it; two days, the critics know it; three days, the public knows it."

Violinist Jascha Heifetz

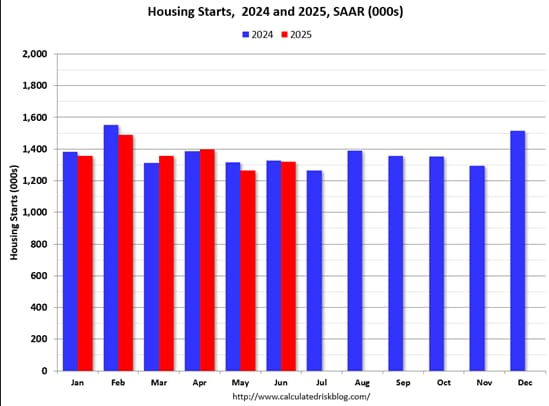

REAL ESTATE

What’s Happening?

From Calculated Risk - Housing Starts still sluggish

sentiment is key - until it shifts positively housing will struggle

it takes longer to afford a house now

that’s why young people that want to buy are frustrated

However Capitalism is doing quite well thank you!

ASSETS

What’s Happening?

mixed returns last week, still a lot of confusion and volatility

people live lives of cash flow, as we teach in CLA you want to understand where consumers really value your advice, for this reason Wall St. is realizing this and really focusing on INCOME as the reason to INVEST… with more and more products that do that for you…

the income that is returned (if not spent) helps JUICE the returns higher especially with Options

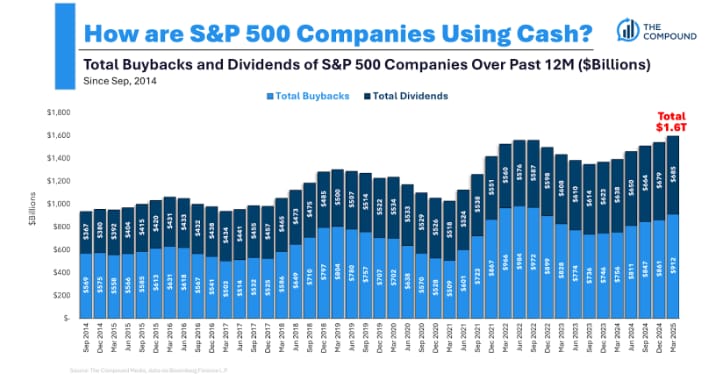

companies with free cash flow are like you, they can spend it or use it to repay debt or INVEST - but their investment is either in their own growth or buying their own STOCK BACK!

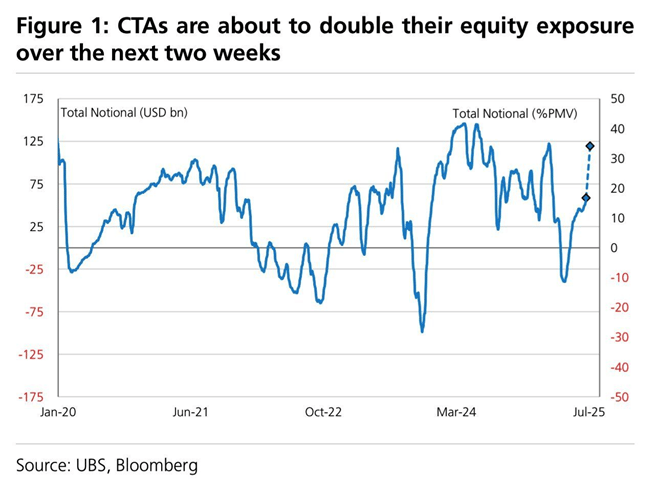

markets by size, Treasuries and BONDs rule…

smart money is about to get BIGLY long…

ON BEING HUMAN

What’s Worth Sharing?

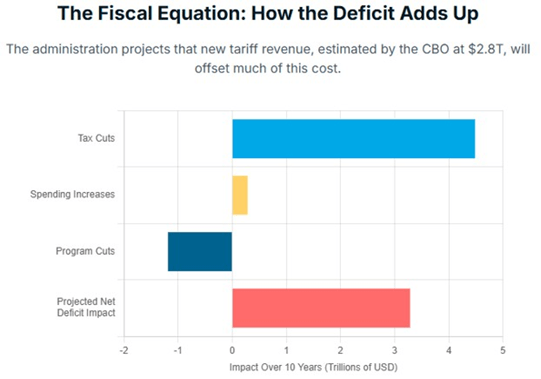

Owning a small business is still the best tax deal in America.

The One Big Beautiful Bill just made it even better.

Whether it’s a $10K side hustle or $10MM business, the new opportunities for tax savings and wealth creation are next level.

Let’s walk through how it works -

— Mitchell Baldridge (@baldridgecpa)

1:50 PM • Jul 13, 2025

an interesting take on the new tax bills:

the ‘savings’ is coming at the cost of something, no free lunches…

DOPAMEMES

And Other Happy Moments…

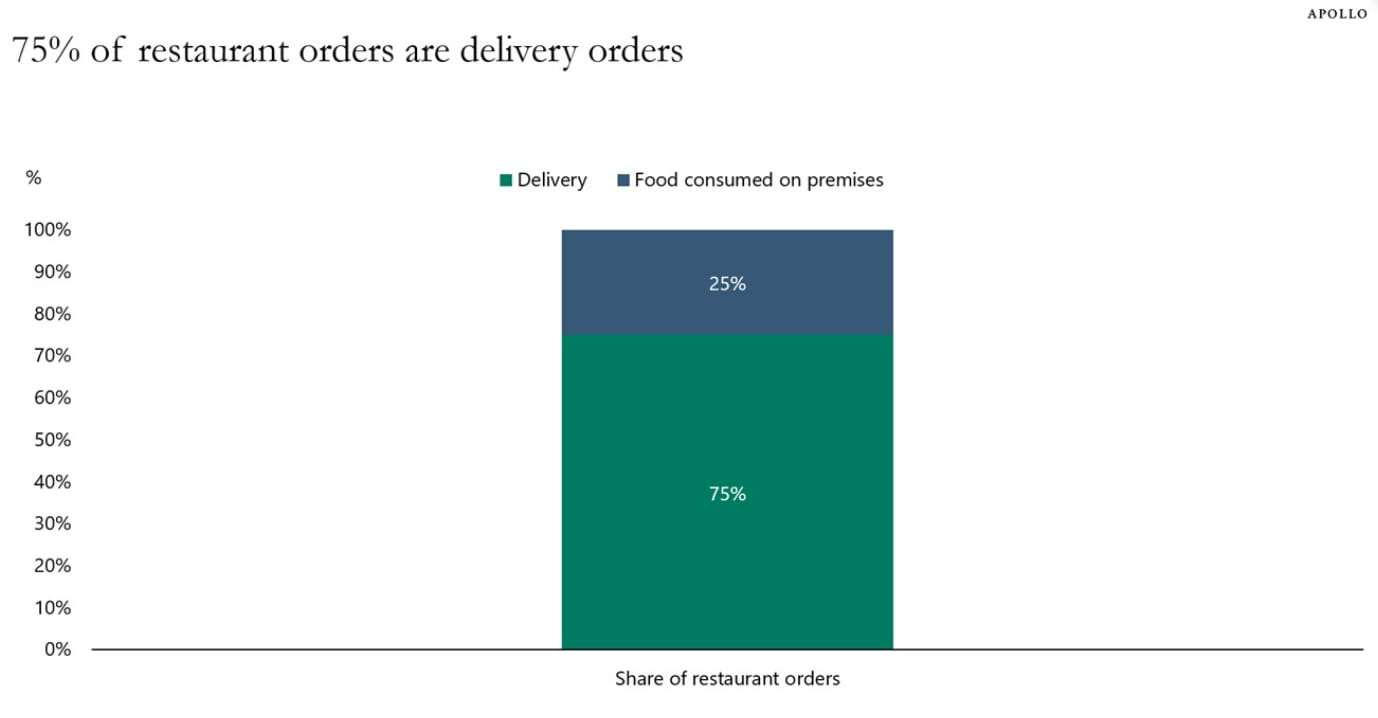

people are ordering in and still post COVID hunkering down…

AI will impact RETAIL more than most industries, see the problem?

Was this email forwarded to you? Sign up here.

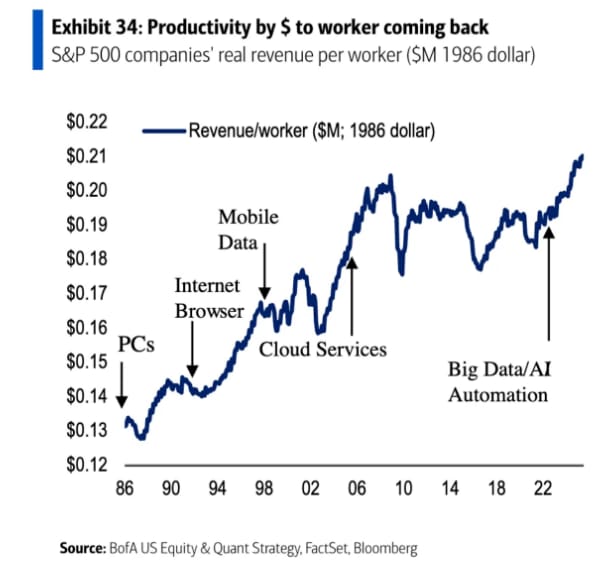

AI

and The Future of Work…

those with jobs are becoming more productive

but maybe losing the ability to write :-)

big TECH is firing rapidly as AI does the work of 10-20 developers

but that makes them more dependent on data centers and information!