- The Borrow Smart Chronicles

- Posts

- Monopoly Taught Me About Risk

Monopoly Taught Me About Risk

and we could also title this the 'Debt Issue' double pun intended

Todd Ballenger

October 31, 2025

"In Monopoly if you don’t take risks,

you’ll end up paying rent to someone that did.”"

At its core, Monopoly isn’t a game about luck — it’s a game about risk, leverage, and ownership. Every time you pass Go, you face a choice: play it safe and save your cash, or take a risk and buy a property. The players who win? They’re not the ones who wait. They’re the ones who take smart risks early, own assets, and let time (and rent) work in their favor. This is true of real estate and most other assets.

🏠 The Real-World Lesson

Life is no different.

If you never take a risk, you’ll spend your life paying rent — not just literally, but financially and emotionally. You might rent your job security from an employer who took the entrepreneurial risk you didn’t, or you might rent a financial future from investors who built a platform to create wealth while you waited. These are all analogs - is there something right now where you are passing Go and thinking ‘I’m gonna play it safe?’

Don’t get me wrong, there is a time to do that. In Monopoly, owning one property changes the game for you. In real life, owning one asset — a home, a business, an idea — changes your trajectory. The most valuable asset you have, is YOU! Make sure you invest heavily there and don’t rent your education, invest in it.

💰 The Cost of Playing It Safe

Here’s the truth no one wants to say out loud:

Playing it safe is often the most expensive decision of all.

Every month you pay rent, someone else earns equity.

Every dollar you park in low-risk “safe” savings, inflation quietly takes its cut.

Every action you avoid because it feels risky could compound someone else’s wealth.

That’s why understanding liability management is key. Borrowing smartly — not recklessly — can be the difference between building wealth and renting it.

🚀 Borrow Smart, Play to Win

Taking risks doesn’t mean gambling. It means playing smart. It means using debt as a tool—not a trap—to build ownership rather than dependency.

The same way a Monopoly player uses mortgages strategically to stay in the game, an individual uses leverage intelligently to grow their balance sheet.

Because the truth is:

You’ll always pay for a property — either through your mortgage or through someone else’s. Unless of course you still live at home with your parents, which is fine if it works for you.

The risk question is: whose wealth are you building when you take an action? That can help open you up to a decision to buy a house now, or invest, in yourself or something else.

🧩 Borrow Smart Insight

Every decision you make with money is a roll of the dice. The goal isn’t to avoid risk — it’s to take calculated ones that buy you ownership, time, and freedom. Life itself is risky.

a BORROW SMART CONCEPT

EPR - Effective Percentage Rate

We teach so many concepts to help lenders become liability advisors. The power of AI is allowing me to code our old calculators in a new way so I can share ideas and have a calculator that will enable you to explore them.

EPR is used in many ways… but one of my favorites is to understand the real price of interest over time. Your NOTE RATE is only your note rate if you pay the exact payment due over 360 months… but what if you pay extra? Paying extra reduces the Effective Rate you are paying. That means that the buyer, not the lender, controls all interest final interest rates paid.

Have a $400,000 mortgage for 30 years at 6.5%; well, you should expect to pay 6.5% over 30 years. What if you paid an extra $100 a month? You just lowered your equivalent net interest rate over the remaining term to 6.10%. Want a 4% mortgage now, then start paying about $550 a month extra, and you’ll pay an effective rate closer to 4%.

You still want to lower that rate whenever you can, but explore, and you’ll get the idea. It’s all about learning to think and speak differently about liabilities.

LIABILITIES

What’s Happening?

we are teaching everyone to play out game, we are just playing it

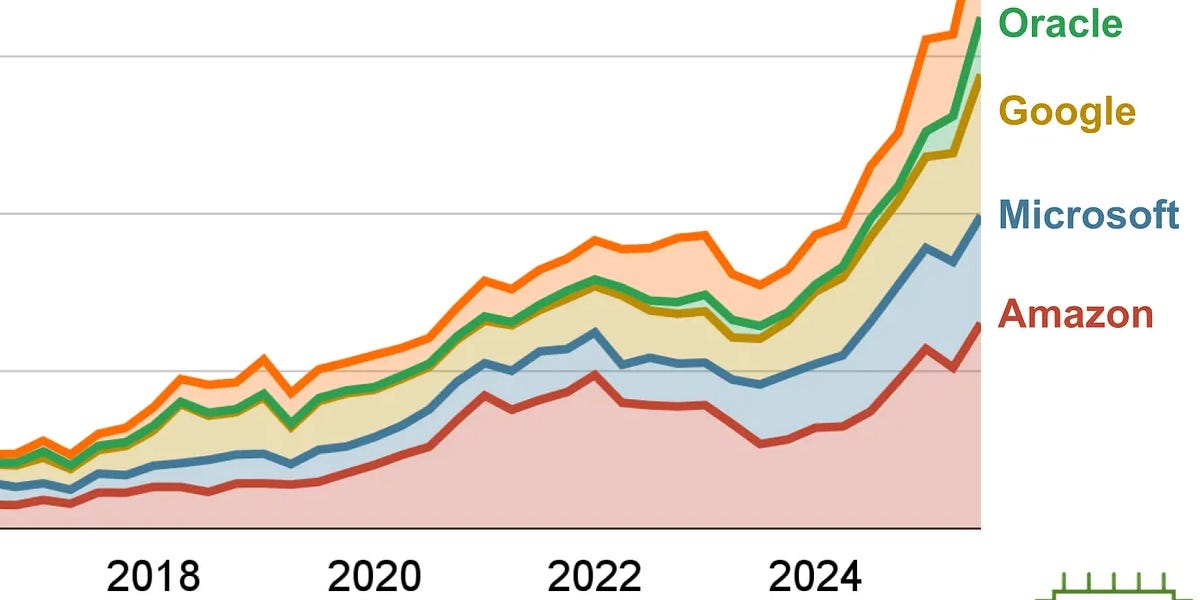

Bigger - this is US DEBT growth since 2000

many investors are using debt now even if they don’t know it

leverage amplifies gains in BOTH directions

If you are not getting into these playlists, you should. I have 180 books left in my library, and I’m done; I’ll be posting a link tree next week for all of them, but save these in your Spotify (or Apple or Amazon) favorites and just hit one a day on your drive to or from work:

REAL ESTATE

What’s Happening?

scary Halloween pranks…

sentiment is tracking well with housing generally

overally we are less happy than we were 10 years ago

and more of us are retiring… drawing on social security

"I make a point to appreciate all the little things in my life, because I learned early that if you don't, you get disappointed a lot. If you do, you might be pleasantly surprised quite often.

I go out and smell the air after a good, hard rain. I re-read passages from my favorite books. I hold the little treasures that somebody special gave me. By keeping my eyes open for unexpected joys, I find the world gives back more than we sometimes think."

ASSETS

What’s Happening?

market has one color lately

we’ll see if there is any red before year end

disruption is everywhere

those using debt to short are getting punished

everyone is all in on technology

and that has paid off being very concentrated

seen differently

ON BEING HUMAN

What’s Worth Sharing?

DOPAMEMES

And Other Happy Moments…

do you understand what’s happening? don’t be a meme…

Was this email forwarded to you? Sign up here.