- The Borrow Smart Chronicles

- Posts

- The First 4 Steps

The First 4 Steps

to managing the greatest wealth (house equity) for the greatest number of people!

Todd Ballenger

October 24, 2025

Don't explain your philosophy. Embody it."

The First 4 Steps to "Borrow Smart": Managing Your Liabilities 7-Step Conversation

Let’s take these a little deeper. As a professional liability advisor, understanding the core process of "Borrow Smart and Repay Smart" is essential for sound financial management. The first four steps of the 7-step borrowing process focus on laying a solid foundation by defining the what and how much of your debt strategy. It’s the most essential part of a Borrow Smart Conversation.

1. Product: How Do You Manage Risk?

This initial step is about the structure of the loan itself and its risk profile. The question, "How do you manage risk?" is behind the Product they choose. You need to look beyond the interest rate and consider the terms, security, and potential volatility of the product.

Importance: A poorly structured loan can expose assets to unnecessary risk or limit financial flexibility. For instance, a loan with a variable interest rate carries the risk of increased payments. In contrast, a loan secured by a critical asset introduces the risk of foreclosure or lawsuit if repayment fails (as noted in the "Safety" concept). Choosing the right "product" is your first defense against unnecessary liability exposure.

2. Payment: How Do You Repay the Loan?

The second step shifts focus to the repayment strategy. The question, "How do you repay the loan?" requires a concrete plan, not just a vague hope that income will cover it.

Importance: A clear repayment strategy directly ties into the financial concepts of Liquidity and Capacity. It forces you to assess your current and projected cash flow to ensure the liability is serviceable without jeopardizing other financial goals. This is about establishing "capacity"—your ability to handle the debt load under various circumstances. A strong plan prevents a productive asset from becoming a financial burden, and it does something few lenders do: it communicates that how the loan is repaid is a massive part of the cost of the liability.

3. Availability: How Much Is Available to You?

Before deciding how much to take, you must know what the market is willing to give. The question, "How much is available to you?" addresses the full extent of your borrowing capacity based on the lender's criteria.

Importance: Understanding your maximum availability provides a benchmark for negotiations and financial planning. It highlights your credit standing, collateral value, and capacity from the lender's perspective. Knowing the ceiling allows you to make an informed decision on the actual amount you should borrow, ensuring you don't unnecessarily deplete future borrowing potential or take on more debt than is prudent for your strategy.

4. Amount: How Much Do You Borrow?

This is the pivotal decision. The question, "How much do you borrow?" is a strategic choice informed by the answers to the previous three steps. It’s rarely about maximizing the available amount, but about optimizing the debt for your specific financial goals.

Importance: The amount borrowed dictates the long-term cost and the degree of Leverage you employ. Taking too little may limit your investment or project potential, while taking too much introduces excessive Hidden Cost (like a higher Effective Percentage Rate, or EPR) and Discipline Risk. The right amount maximizes your potential Return while keeping the liability manageable, striking the crucial balance between debt utilization and financial safety.

Borrowing without a Solid Framework is like…

a BORROW SMART CONCEPT

Why Manage Liabilities?

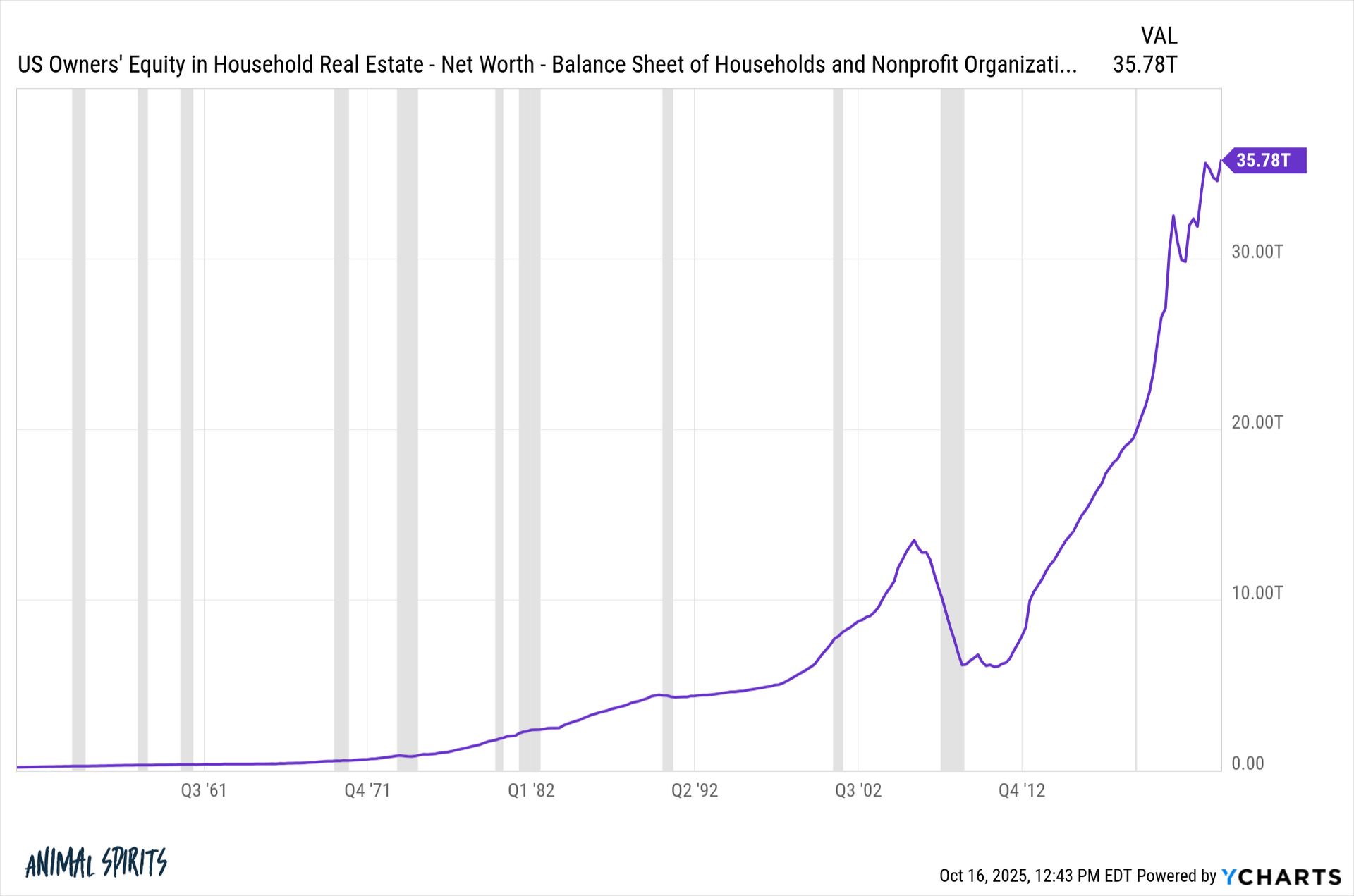

For the majority of American households, home equity is not just a number on a balance sheet—it’s one of the most significant sources of wealth and cash flow flexibility available. Understanding and managing this equity smartly is critical to building long-term financial security and wealth.

1. House Equity as a Primary Source of Net Worth

According to the foundational concepts in Borrow Smart, Repay Smart, and house equity, the difference between the home's market value and the remaining mortgage debt is the most common form of wealth in the United States. This makes it a central asset in household financial planning. Yet many borrowers focus solely on paying off their mortgage without understanding how that equity could be used more effectively.

2. The House as Both an Asset and a Liability

A house represents both an asset (the property itself) and a liability (the mortgage). This dual nature places the home right at the intersection of a borrower’s financial life. The key to “borrowing smart” lies in understanding how the liability (the mortgage) can be used to control and enhance the value of the asset (the home) over time.

3. Using Equity to Manage Cash Flow

Home equity is often seen as a “silent” part of wealth—it grows quietly as mortgage balances decrease and home values increase. However, that equity can be used to manage cash flow, primarily through strategic refinancing, home equity lines of credit (HELOCs), or reverse mortgages later in life.

This liquidity can be redirected to:

Pay off higher-interest debts

Invest in other appreciating assets

Fund business ventures or education

Create a buffer for retirement income

In this way, liability management becomes a form of cash flow management. It’s not about having zero debt—it’s about having smart debt.

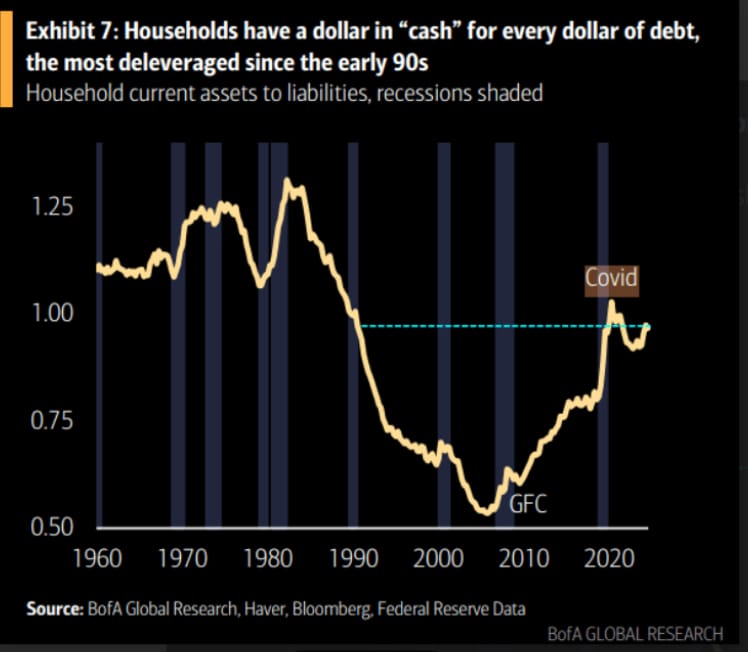

Housing is the majority of wealth for the majority of people

LIABILITIES

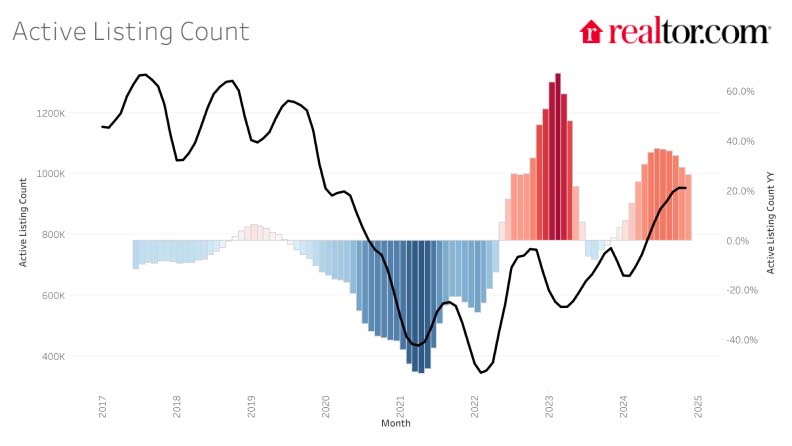

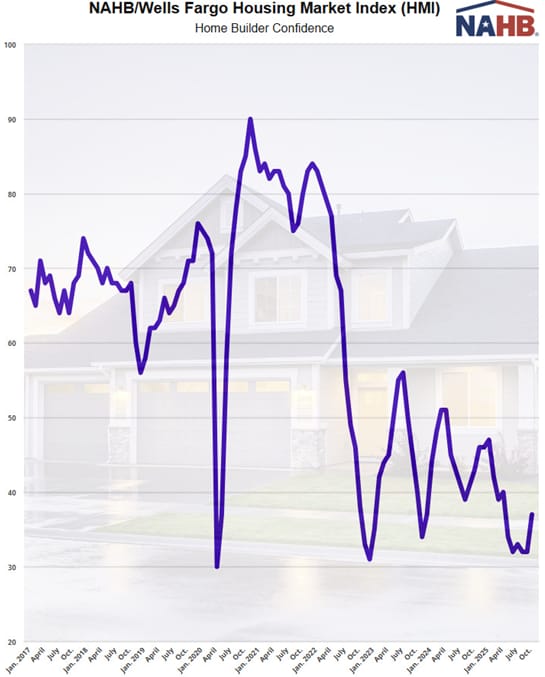

What’s Happening?

Torsten Slok - defaults are coming down as rates come down

ON BEING HUMAN

What’s Worth Sharing?

Some spend life chasing the perfect wave. Others become the reason someone else finds theirs

— Ryan Cey (@RCEY28)

12:35 AM • Oct 18, 2025

may attention when you drive!

DOPAMEMES

And Other Happy Moments…

Was this email forwarded to you? Sign up here.