- The Borrow Smart Chronicles

- Posts

- The House, Borrowing and

"Success is being excited to go to work

AND being excited to come home."

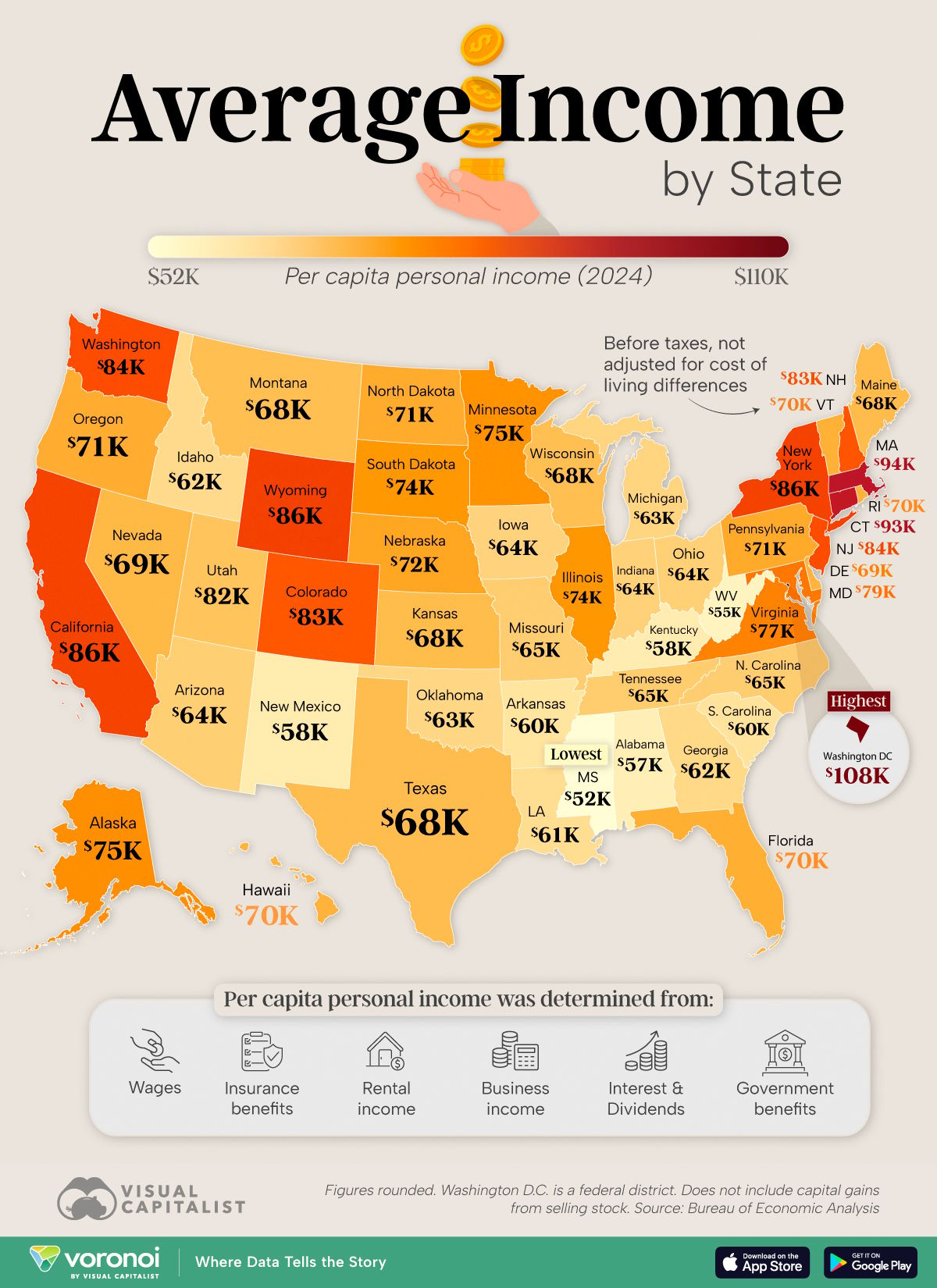

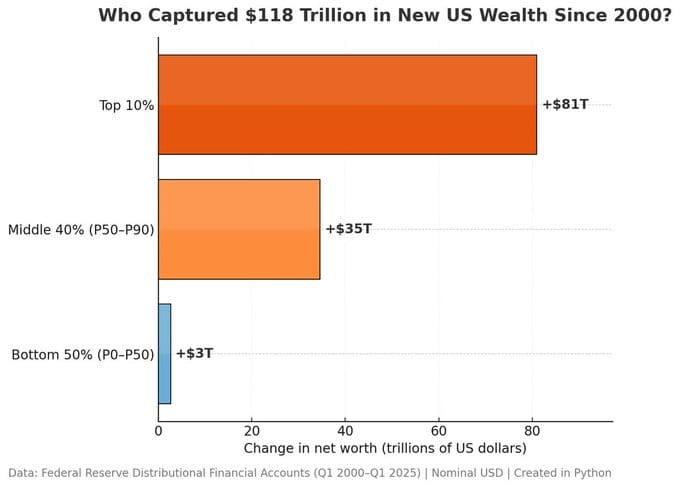

For the first time, “other financial assets” — stocks, bonds, mutual funds, and similar investments — have surpassed the home as the single largest store of consumer wealth, making up 43% of all household assets compared to homes at 27%.

These ‘other financial assets’ are often managed by financial advisors, yet who manages the wealth in the house?

Mortgages still dominate borrowing, representing 67% of total consumer liabilities. This mismatch reveals a powerful opportunity: trillions of dollars of wealth inside the house and against that asset - leveraged borrowing. There is much you can do!

Managing the house strategically — both as an asset and as the source of the largest debt — can free up cash flow, reduce borrowing costs, and potentially redeploy equity into higher-performing investments over time.

In other words, the biggest lever for improving consumer balance sheets is still the one with a front door and a roof.

Here’s a simple example:

A homeowner has:

$1M in total assets (PS - this is Level IV Wealth - more on this next week)

$330k in other financial assets (stocks, funds, etc.)

$470k in home value

$200k in pensions, deposits, and other assets

$270k mortgage at 3% interest

They are paying $300 extra each month on their mortgage.

The result: They’ll own the house in about 21 years, saving about $40,000 in interest.

Working with a financial advisor, they believe they can earn 9% net after tax during that same 21-year period.

They invest $300 a month in ‘other financial assets’ and in 21 years they have: $215,360 in growth, AND their house value will be the same either way. The house doesn’t know how much equity it has inside it, it doesn’t ‘appreciate’ equity - that’s a joke!

The result: they can pay off their remaining mortgage balance of $107,000 in 21 years and have over $108,000 left over…

This Lowers real cost of this debt by 40%

Faster growth of financial assets, could be used to pay off the house much sooner if desired, and be used for ‘other financial assets’

More liquidity and flexibility, instead of tying cash flow into rapidly paying down low-yield home equity and locking it up inside the house.

This is a “borrow smart, repay smart” principle — manage the home asset and debt deliberately so it supports the growth of your larger wealth portfolio rather than draining it.

There are other possibilities, but this one is a surprisingly real example where consumers are almost always paying a little extra toward their house without realizing the cost.

If you need a question for a financial advisor, just ask them to ask every client that comes in for an annual (or quarterly) review - how much extra they are paying each month toward their mortgage.

NOT a BORROW SMART CONCEPT… just for fun.

Use AI to Create Custom Stories to Engage a Client or Referral Partner

How to create these?

Why create these?

Storytelling That Wins Referral Partners

A new referral partner is more than a contact — they’re your voice in new markets. To win their attention, skip the bland welcome kit. Give them a story where they’re the hero.

Gemini Storybooks makes this simple. You craft a short, illustrated tale where their journey and your solution meet.

Why it works:

Memorable: Cuts through inbox noise.

Personal: Shows you understand their business.

Clear Value: Weave benefits into the plot.

Exciting: Builds real enthusiasm.

Shareable: Stories travel fast.

Example: The Case of the Missing Homebuyer— your partner is a detective hunting quality leads. Your program is the clue that cracks the case.

This could be a fun way to include a Realtor’s name and company and engage you in a way that stands out.

Start with a story they’ll remember — and share.

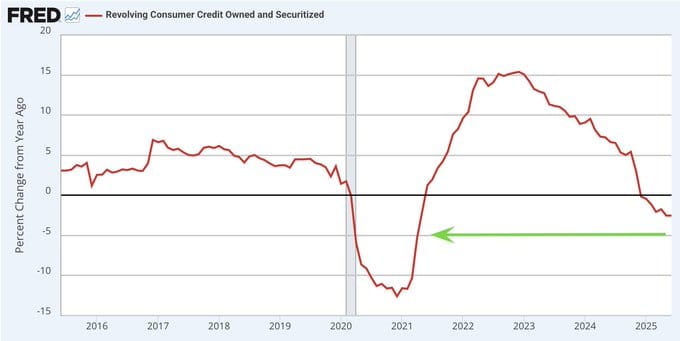

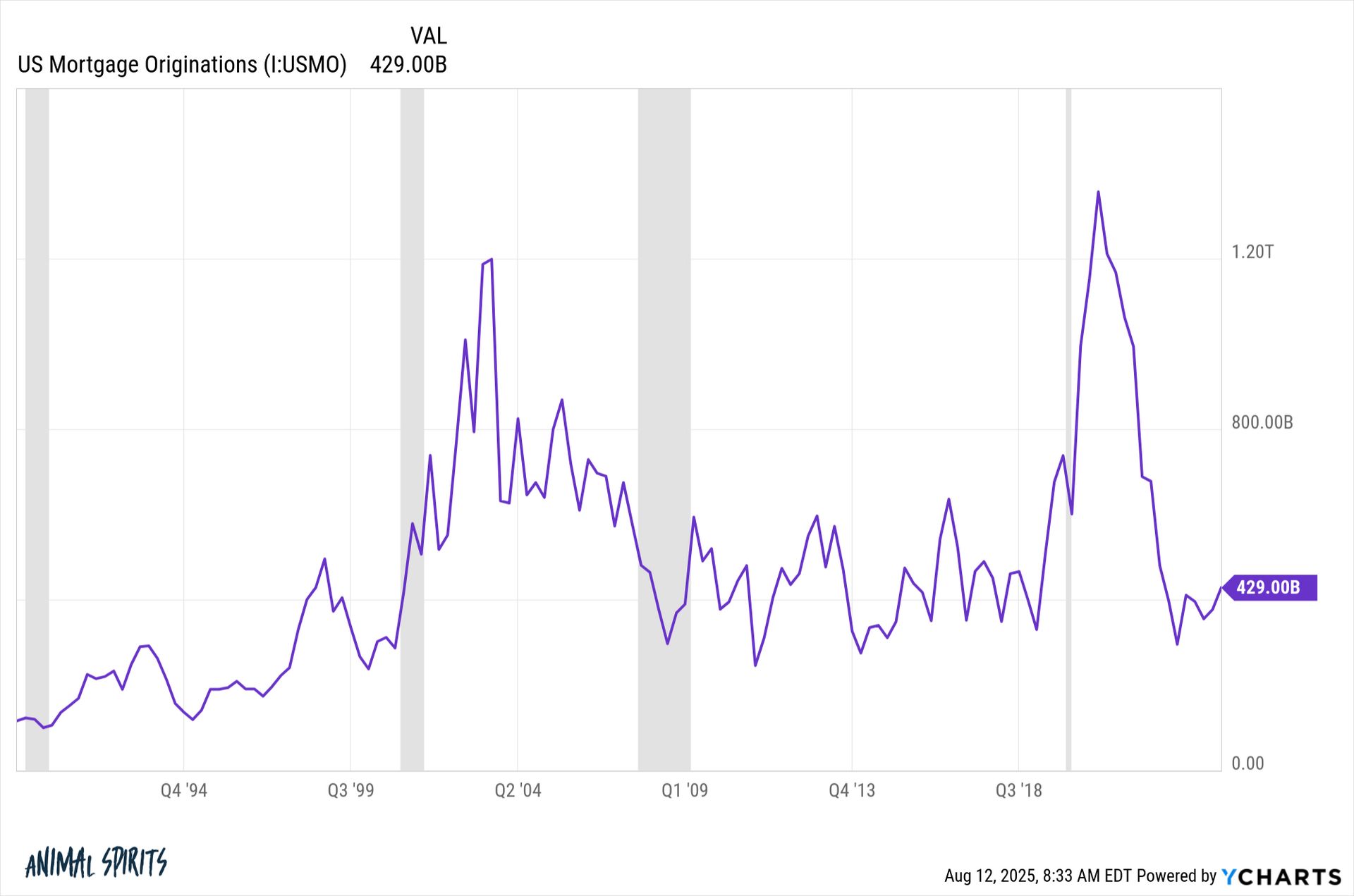

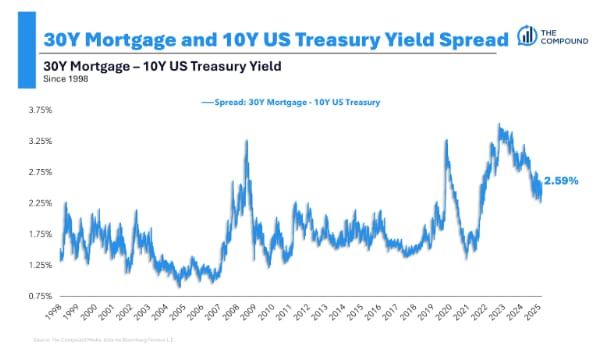

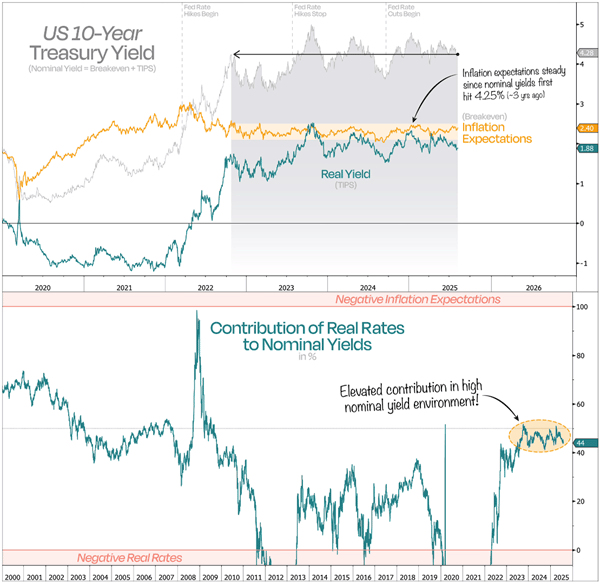

LIABILITIES

What’s Happening?

consumers are still shying away from borrowing when they have a choice

people would make more income if they could, the fix for housing is not lower rates as much as it is lower cost of housing!

the rates part is happening

and mortgages are being paid on time

but new loans are light (but trending up)

and spreads are helping rates come down

“real yields — they’re the only thing that can actually push nominal yields down”

Duality Research

income can go up, but not likely to solve housing / borrowing needs

the way to do that is start a side hustle!

Great clip on the Federal Reserve.

Show this to everyone you know.

— The General (@1776General_)

11:49 AM • Aug 8, 2025

H/T - Will Ballenger

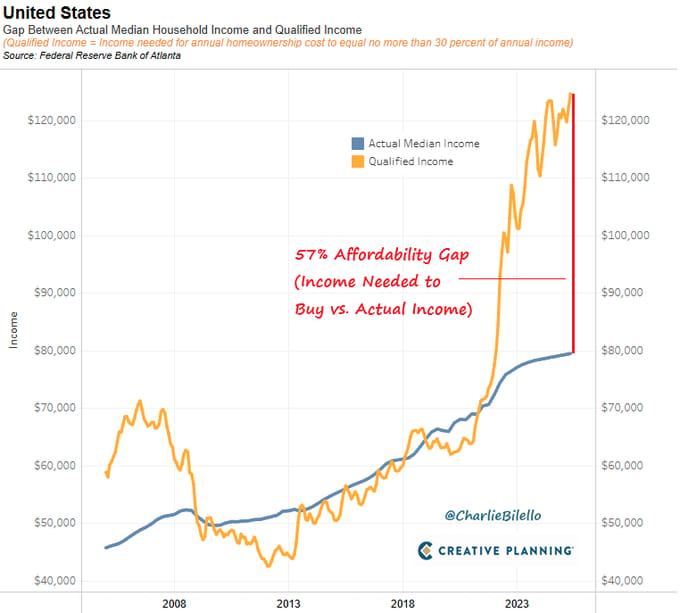

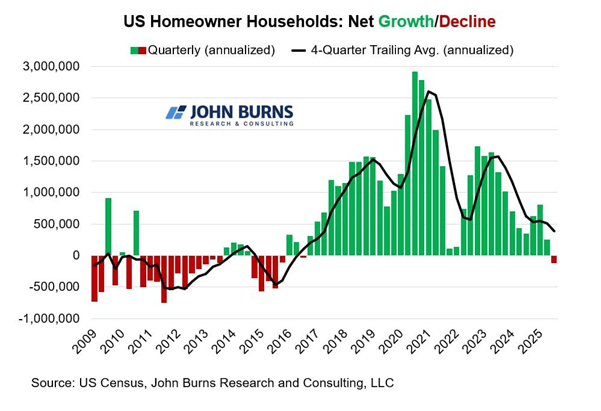

REAL ESTATE

What’s Happening?

starting to look like a recession now in housing overall

listing going up is one way to get housing prices down

month by month this years sucks a little bit more than last year :-)

but sentiment is shifting!

"I make a point to appreciate all the little things in my life, because I learned early that if you don't, you get disappointed a lot. If you do, you might be pleasantly surprised quite often.

I go out and smell the air after a good, hard rain. I re-read passages from my favorite books. I hold the little treasures that somebody special gave me. By keeping my eyes open for unexpected joys, I find the world gives back more than we sometimes think."

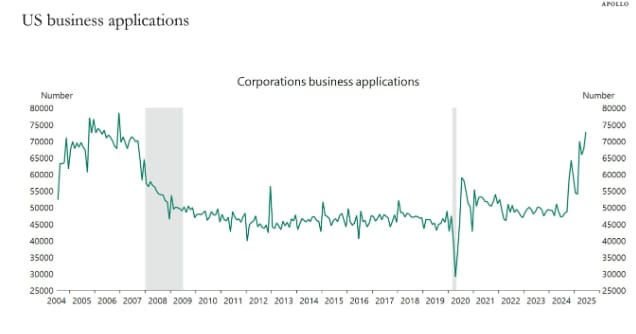

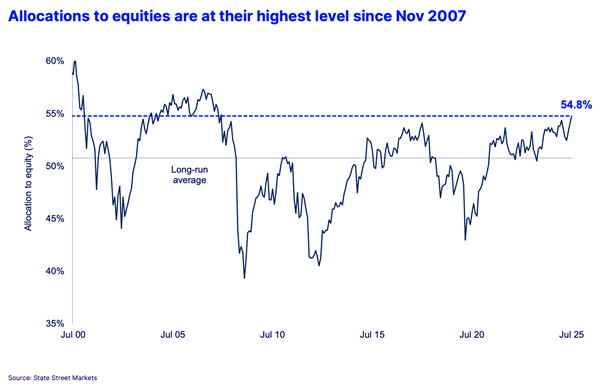

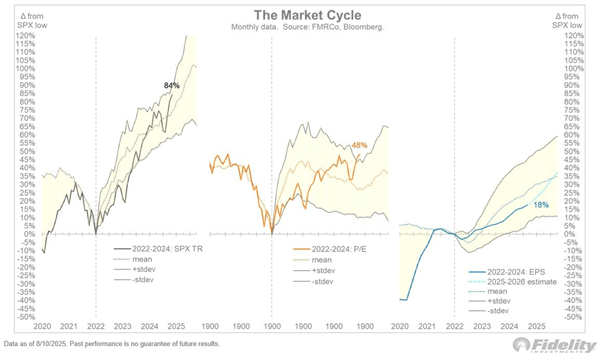

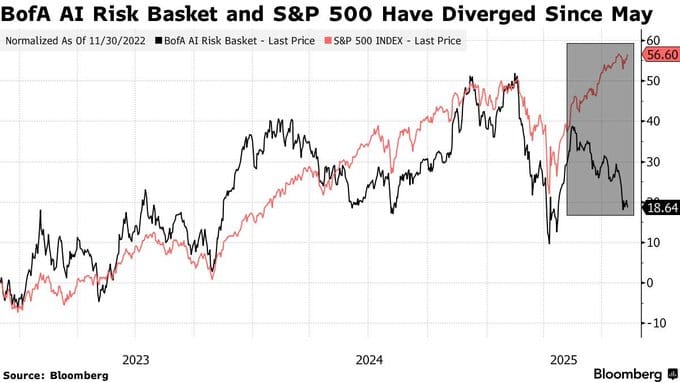

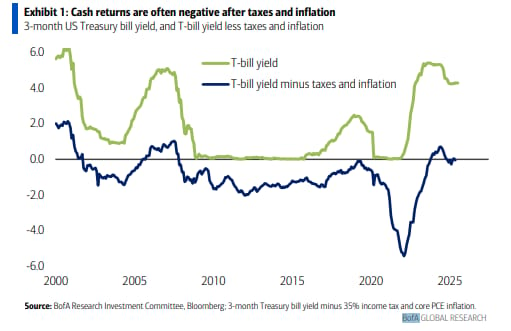

ASSETS

What’s Happening?

seems fair!

concentration happens …

but this is a sign of a lot of liquidity in the world…

and that money is going into stocks too!

liquidity is everything, because with enough of it even shit floats!

we are at an interesting late stage of one cycle, but could be rotating to another

we are moving toward a series of volatility

HIGH RISK and RISK are diverging

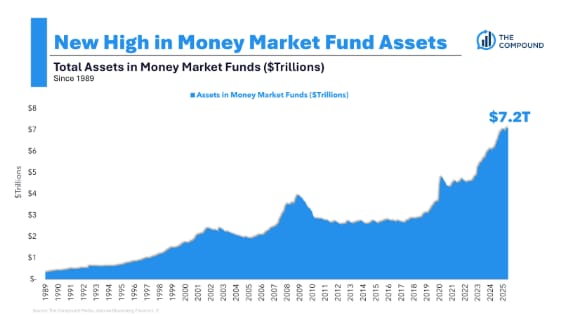

holding cash is not going to work longer term…

DOPAMEMES

And Other Happy Moments…

I want to meet this guy!

Was this email forwarded to you? Sign up here.