- The Borrow Smart Chronicles

- Posts

- The Housing Crisis Is Real

“The best investment on Earth is earth

(land and real estate).”

Housing in Crisis, or Opportunity? It Depends.

It’s top of mind again, this thing we call estate. Maybe it never left.

The story of housing today isn’t just told through headlines or Zillow listings; it’s lived in family budgets, financial decisions, and the psychology of whether the American Dream still feels within reach. And lately? For many, it doesn't.

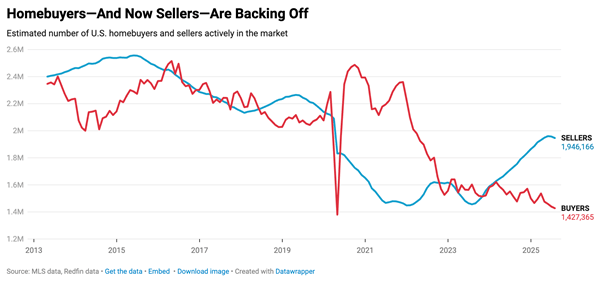

According to Redfin's chief economist Daryl Fairweather, the market is shifting. Supply is climbing. Demand is constrained. Charts tell the truth in a thousand pixels: the housing market feels perched, uncertain, and vulnerable to gravity. It also feels like it is ready to run hard and solve for all that pent-up buying demand.

But if we pause, zoom out, and shift our focus to fundamentals—not fear—what we see is something far more empowering: a system overdue for a reset, and with it, new pathways for creating wealth through smart housing decisions (also known as liability management).

Why Housing Feels Broken

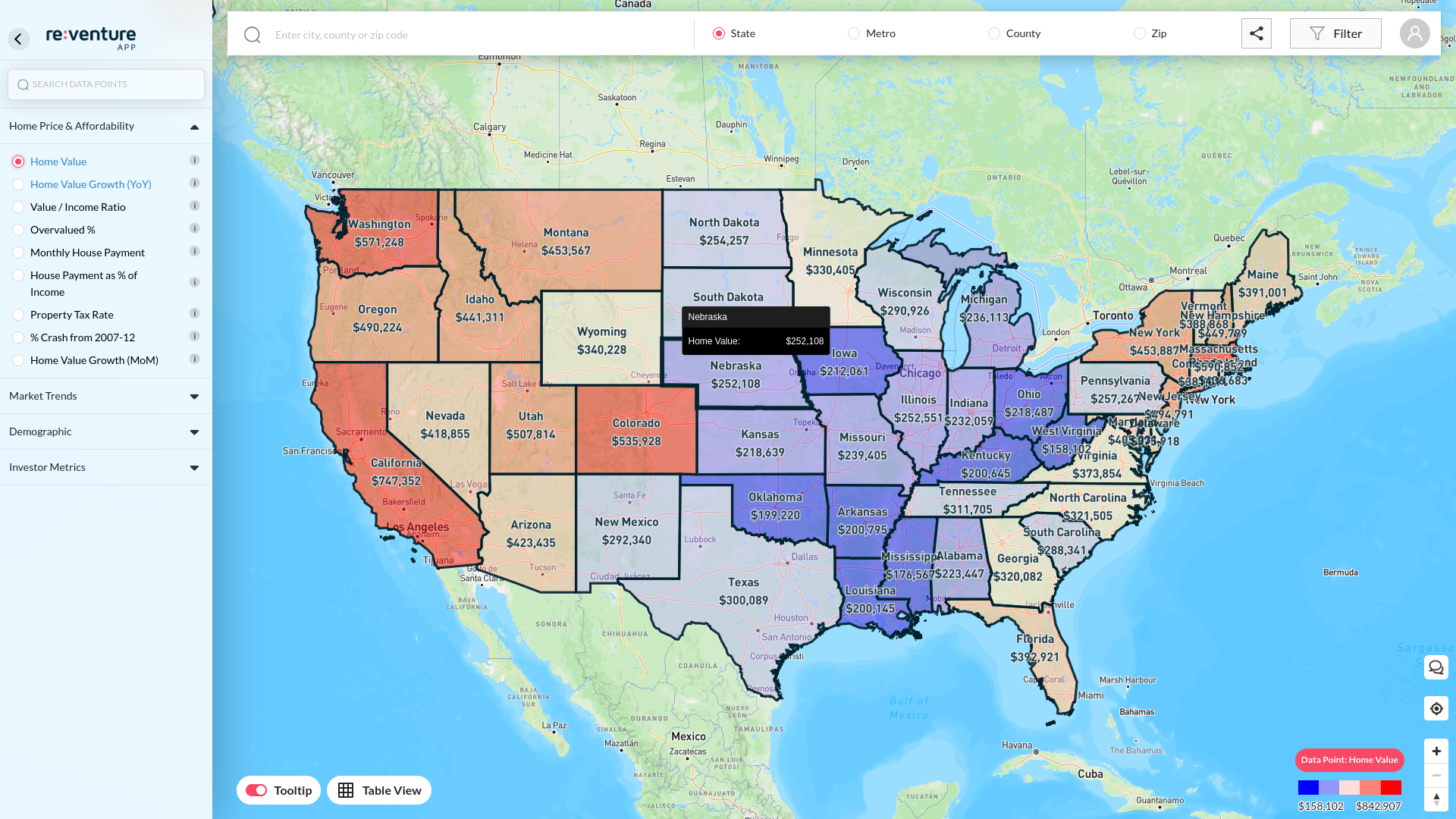

Let’s name the elephant: affordability is a crisis. The median age for first-time homebuyers has crept up to nearly 40. Homeownership, once a rite of passage in your 20s or 30s, now feels like a luxury. In cities like Austin or regions of Florida, values are already cooling. In California, Proposition 13 and the mortgage lock-in effect are keeping homeowners tied to low-rate loans and preventing healthy market movement.

Yet here's the paradox: in many places, homes are trading below replacement cost. This means buying existing homes—renovated or not—can represent a discount to building new. For those with the cash flow and strategy to leverage this, it’s a buying opportunity, not a burden.

The Financial Mind Game of a Home

Owning a home is both consumption and investment. And that duality is where most people stumble.

When you remodel your kitchen, you might enjoy it, but you may never get that money back. The payoff is emotional. Meanwhile, adding an ADU or solar might offer real ROI, increasing utility or lowering costs. Sorting these into “investment” or “consumption” is vital. Most people don’t. But financially literate buyers do—and they win the long game.

That’s why we need to stop seeing homes purely as assets or liabilities. As we say in my book Borrow Smart, Repay Smart, your house address is always at the intersection of safety, liquidity, and return. It is both shelter and strategy. And managing it smartly, especially your liabilities, can turn housing from a weight into a wealth engine.

The Big Lie: Pay Off Your Mortgage as Fast as Possible

No. Not always. In fact, often the most brilliant move for most is to carry a long, big mortgage.

Why?

Because mortgages act like inflation hedges. As inflation increases the cost of goods, your fixed mortgage payment becomes cheaper in real terms over time. Meanwhile, the value of your home tends to rise with inflation. This is the wealth effect at work. You’re building net worth on both sides of the balance sheet—your asset is going up, and your liability is effectively going down.

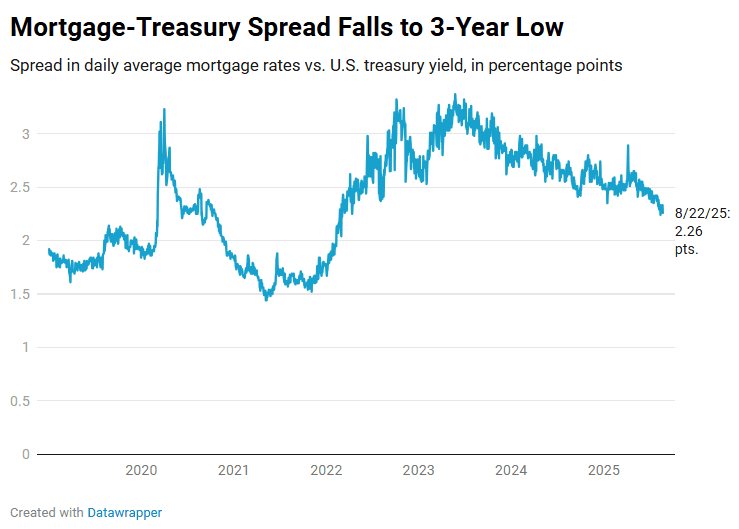

Did you know the average mortgage rate in the US today is below the inflation rate? Do you know what that means? You are being paid to have a mortgage in real terms.

Ric Edelman’s classic essay “11 Reasons to Carry a Big Long Mortgage” backs this up—and was updated by me to reflect today’s realities. It’s not about reckless borrowing. It’s about smart leverage, liability management, and cash flow preservation.

The Silent Killer: Poor Liability Planning

Housing isn’t in crisis because the house is inherently a bad investment. It’s because we lack a framework to manage borrowing and housing wisely. Financial advisors manage wealth, and realtors sell real estate. What do lenders do? They either sell money OR they manage liabilities.

Tools like the 3-Sided Balance Sheet help reframe how we think about our mortgage—not just what it costs monthly, but how it impacts safety, liquidity, and return over time. Smart borrowers build plans around these three dimensions.

And today, tools like Mortgage Coach, and our Liability Advice Engine help to show the value of your advice by optimizing liabilities in the same way a financial advisor might optimize assets; there’s no excuse not to bring your housing strategy into the same conversation as your retirement plan or portfolio management.

Final Word: We are on the Edge of a Transformation Economy

Real estate didn’t break affordability; it broke belief in the future for many. That’s what this moment is really about. When people feel the ladder’s been pulled up, anger and apathy fester. That’s the root of our political division. Of our generational frustration.

But it doesn’t have to be this way. There are ways to help anyone buy a house. This week we showed a case study of a parent with a highly appreciated property and no mortgage using that equity via a reverse mortgage to help both their children buy their own houses - essentially an advance on their inheritance!

Reframing housing as a dynamic tool for wealth, not just a static symbol of arrival, opens the door again to the American Dream. And for those willing to Borrow Smart, Repay Smart, and think like both a house owner and a house investor, the future is still very much for sale.

If you're in the housing market—or advising someone who is—ask better questions. Use better tools. Understand the forces at play. And borrow like your future depends on it.

Because it does.

Want to come learn with us - the door is open.

LIABILITIES

What’s Happening?

equities taking up the top spot on non-real estate assets

rates trending down

another look at 10 year

The key has been a lack of fear in repaying US debt, and compressing spreads

"And now that you don't have to be perfect, you can be good."

REAL ESTATE

What’s Happening?

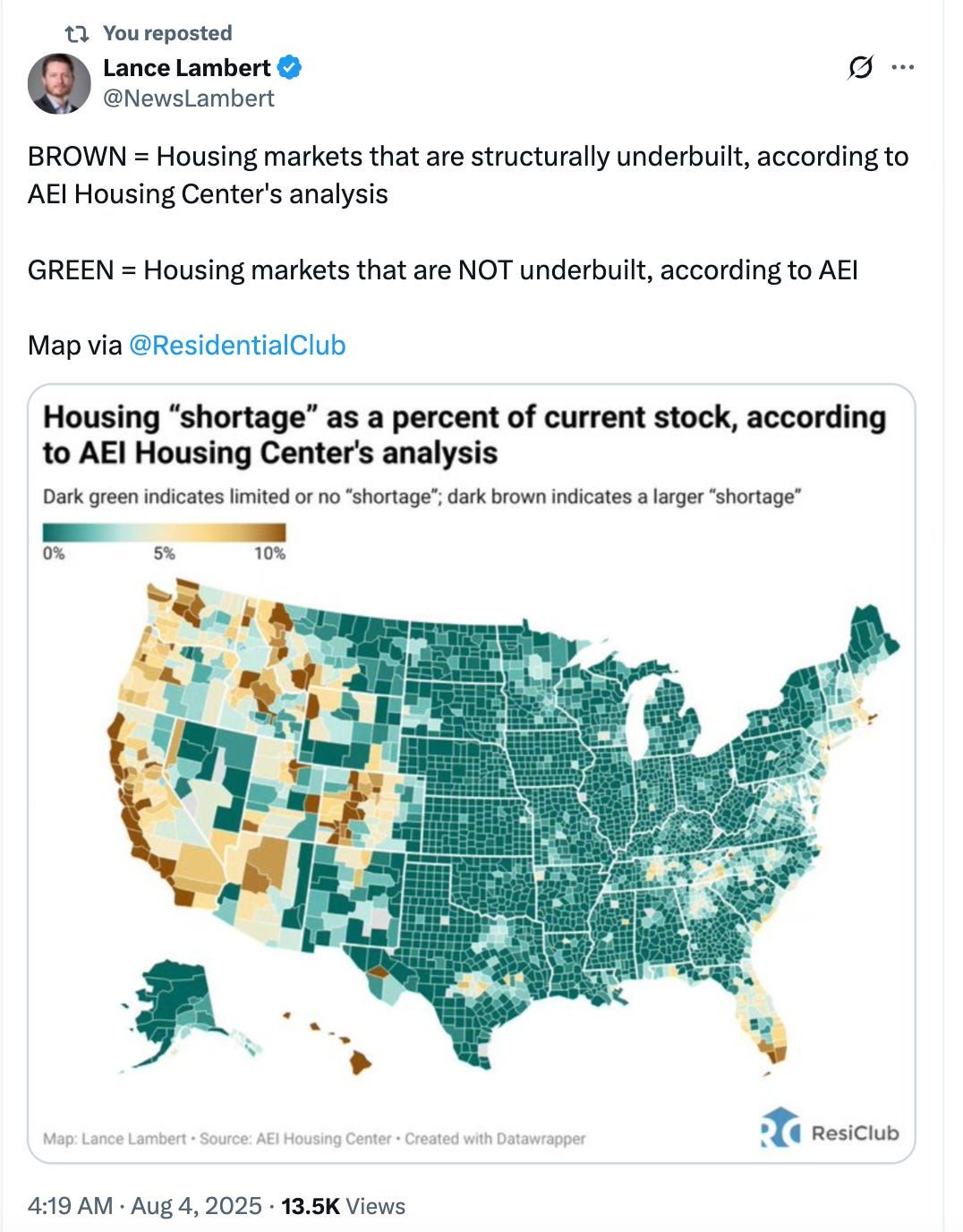

inventory low

purchases falling through at highest level in 10 years

prices go up and down, but mostly up

affordability starting to trend up!

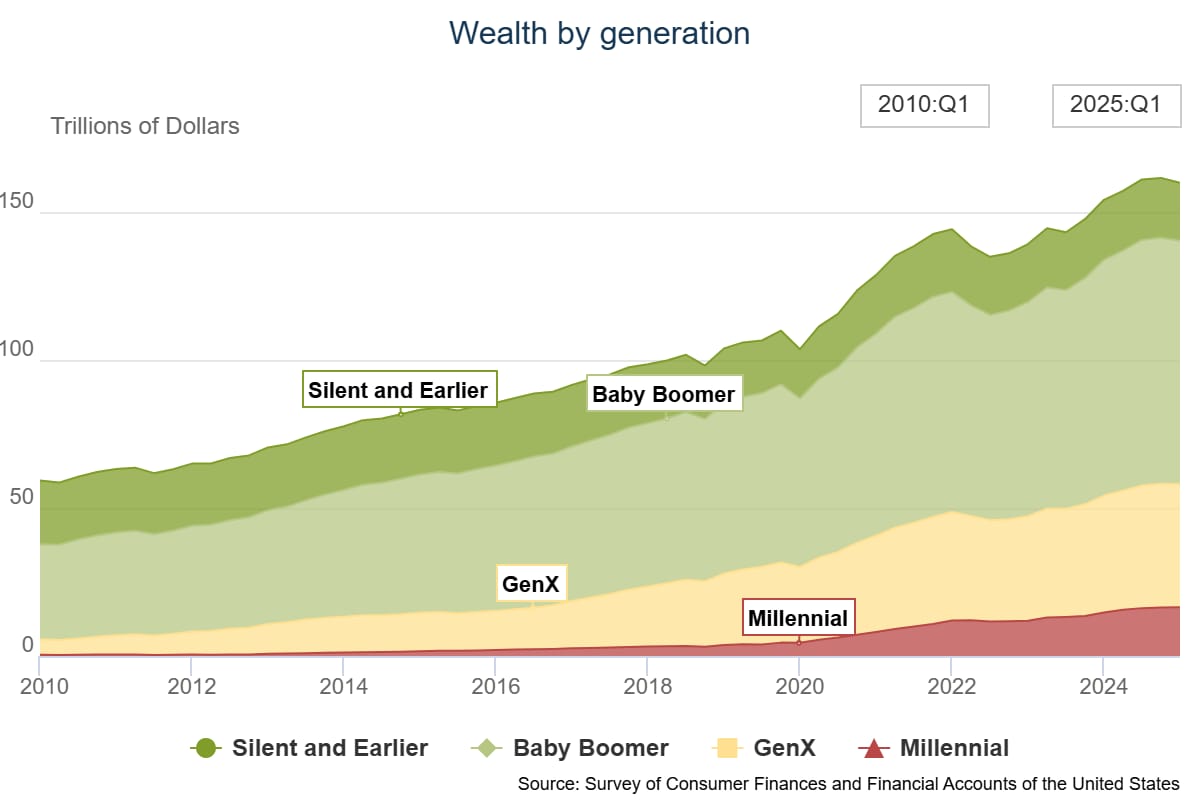

parents have a lot of wealth to transfer to their kids to buy houses

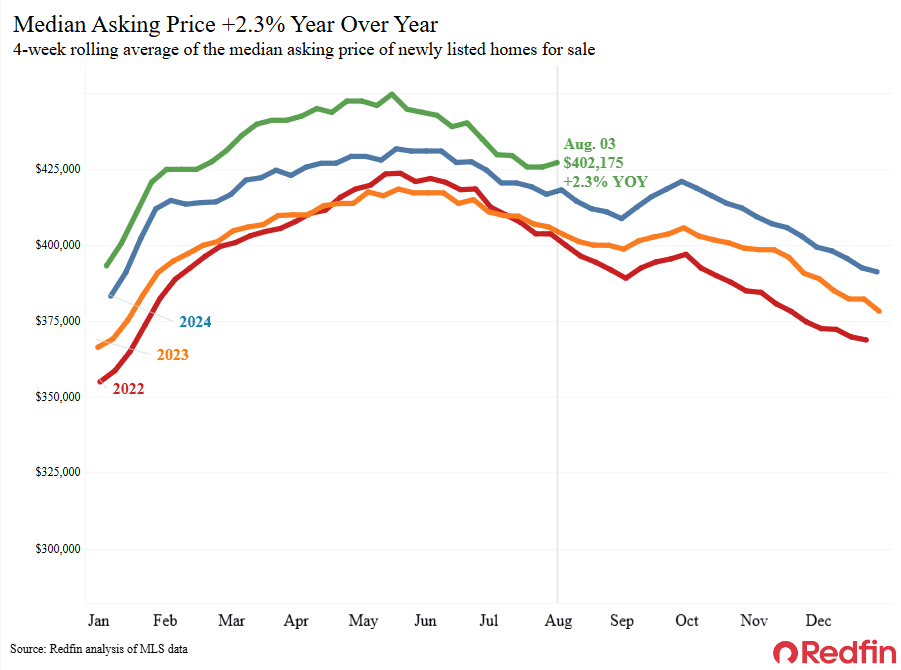

and asking prices are still trending down this time of year but above prior years

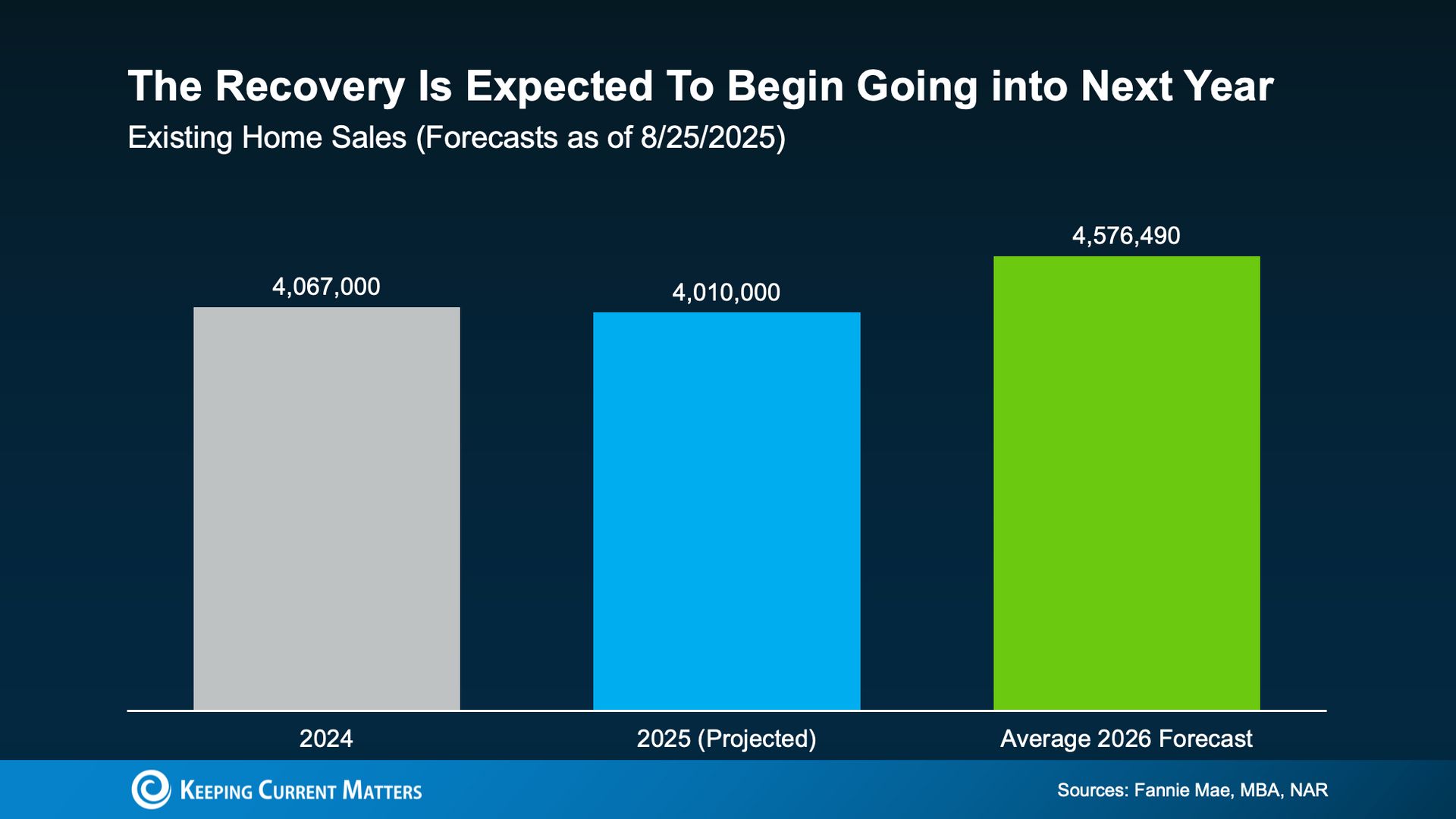

from KCM, sentiment vibes are improving across the board

approaching 40

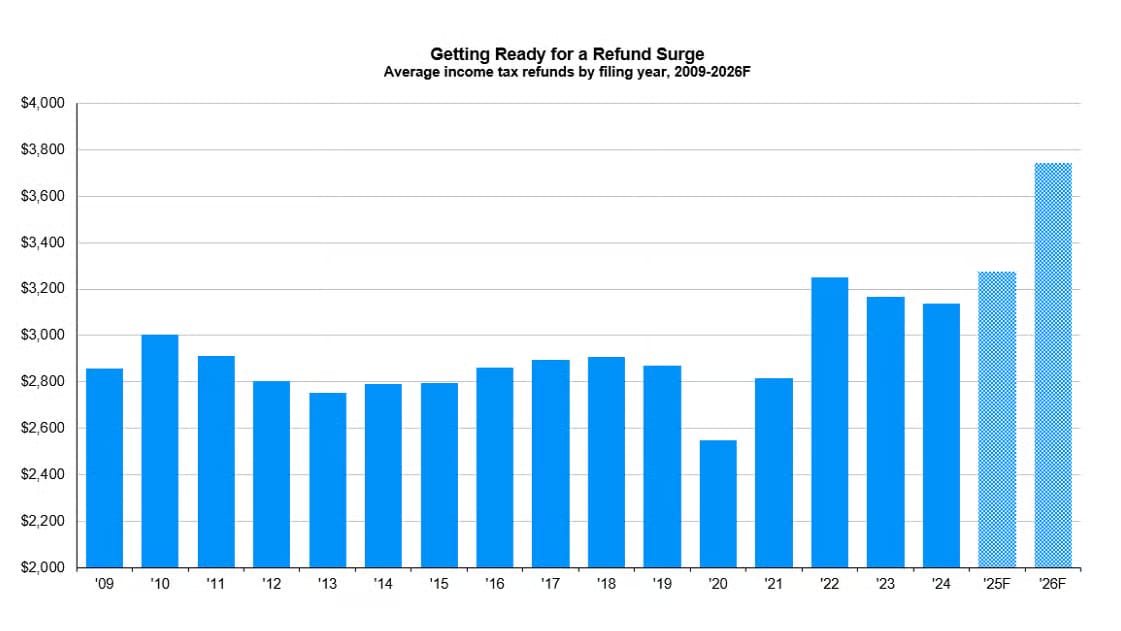

tax refunds can be a source of down payments for smaller starter homes

"When you plant anything,

you are essentially believing in your tomorrow."

ASSETS

What’s Happening?

stonks go up

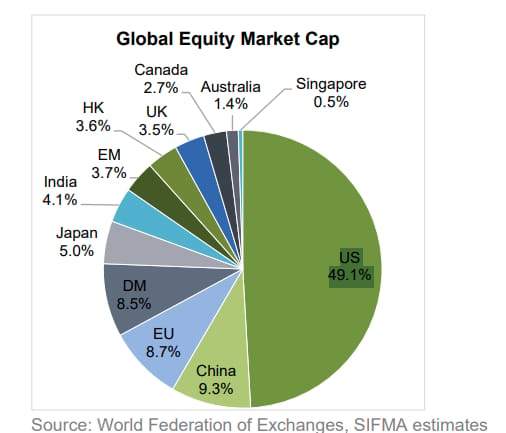

mainly in the US

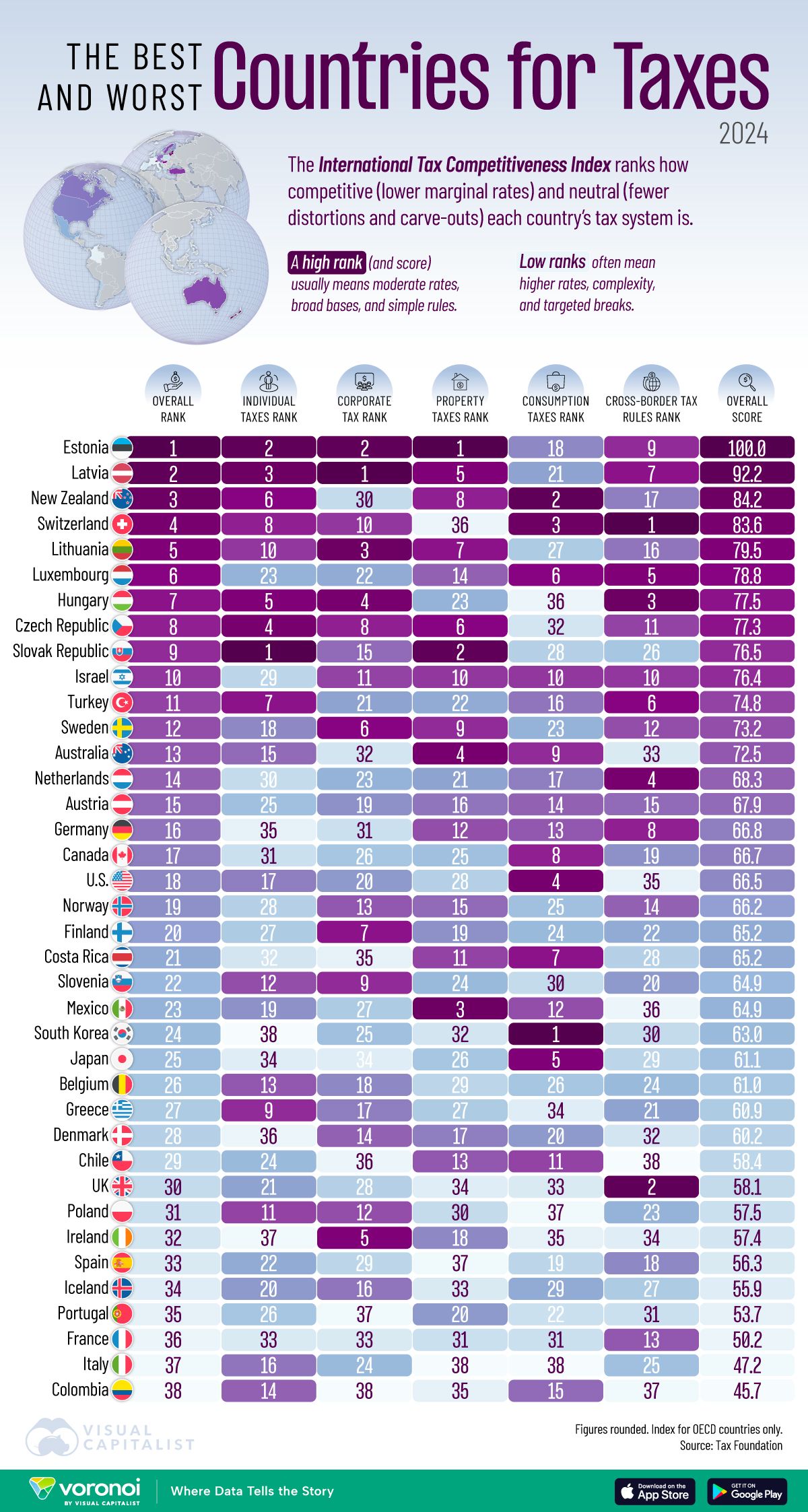

but I may move to Estonia

when you borrow you borrow from the future

and we are trying to distribute the loan payments to other countries

another look at who is paying those taxes

more stocks are going up, breadth is widening

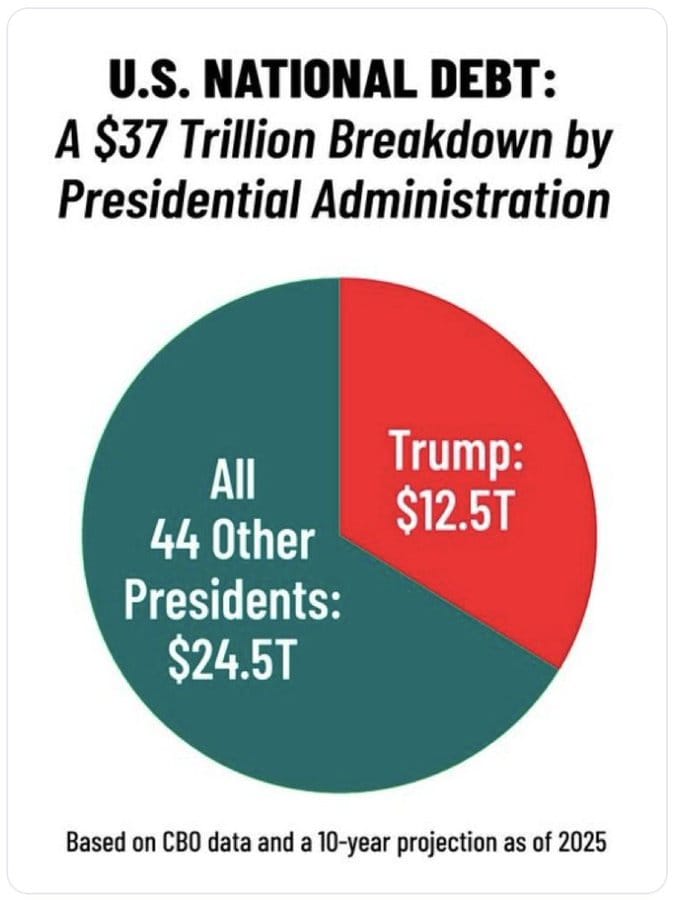

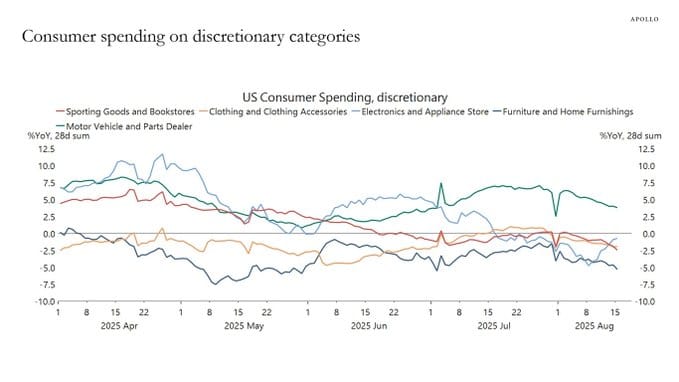

consumers are getting tighter in some categories

ON BEING HUMAN

What’s Worth Sharing?

I needed to hear this today 🙏😊

— G-PA (@IndianaGPA)

6:19 PM • Aug 22, 2025

DOPAMEMES

And Other Happy Moments…

Was this email forwarded to you? Sign up here.