- The Borrow Smart Chronicles

- Posts

- The Market Isn’t Testing Your Sales Strategy. It’s Testing You.

The Market Isn’t Testing Your Sales Strategy. It’s Testing You.

How Borrowing Fuels the Economy: The Crucial Role of Liquidity in Stock Market Dynamics

Todd Ballenger

August 01, 2025

“You don’t know how strong you are until being strong is your only choice.”

Stop Hiding Behind Bagels

Most loan officers think becoming “great” is a game of realtors, phone calls, and dropping off bagels. It’s safe. It’s predictable. It’s what you’ve always done.

But here’s the truth:

The real edge — the one that endures through market cycles and actually separates the elite from the average — isn’t about the number of bagels you deliver.

It’s psychological.

The Market Isn’t Testing Your Strategy. It’s Testing You.

The market doesn’t just test your patience; it tests your ability to sit still when the world panics. It doesn’t just reward intelligence; it rewards resilience.

And most importantly — the market PUNISHES emotional fragility.

If you can’t manage your fear, your hesitation, your “what if it doesn’t work?” loop — it doesn’t matter how good your strategies are. Everything takes time in time.

Your Brain Is Lying to You.

Behavioral finance has proven something uncomfortable:

Humans aren’t wired for compounding. We’re wired for survival.

That wiring whispers:

“Protect yourself.”

“Don’t risk it.”

“Stay where it’s safe.”

Which feels smart in the moment… but is exactly why most of us never break through. We miss the simple fact that everything in your life (good or bad) compounds over time.

Because here’s the paradox: building a business that thrives long-term often requires the opposite instinct — patience, action, and calculated consistency.

In slow markets, you’re handed a gift: time.

Time to plant seeds in new places — like financial advisors.

Time to build the referral machine everyone else will envy when the market roars back.

But the question is: are you wired for that? The answer is: You are not.

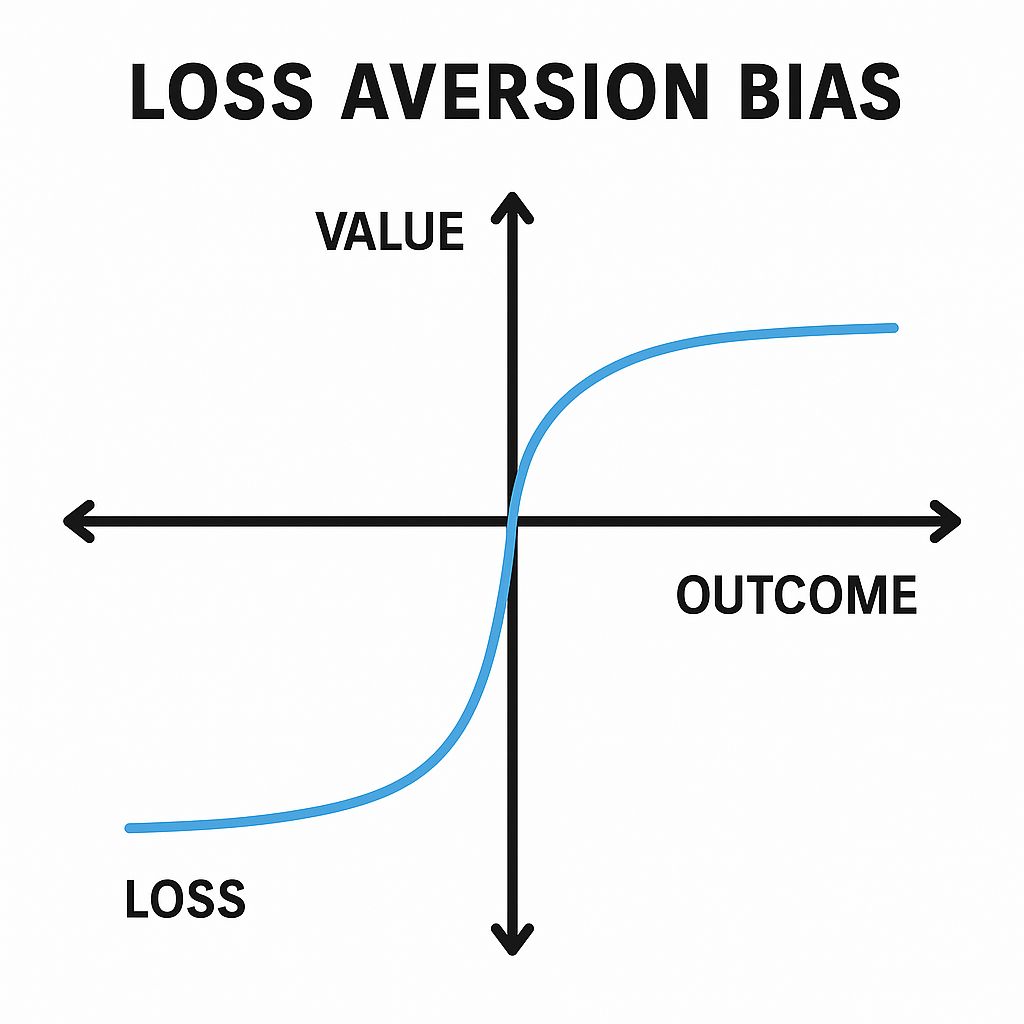

Loss Aversion: The Silent Business Killer.

Here’s the science:

Losing hurts twice as much as winning feels good.

A 10% drop in referrals feels like a gut punch.

A 10% gain? Barely registers.

That’s why most of us cling to what’s “safe.”

They don’t avoid new opportunities because they don’t understand them — they avoid them because they don’t want to feel the sting of trying something new and looking foolish.

The Truth About Discomfort

Loss aversion makes you:

Focus too much on the short term.

Hesitate on the one big move that could change everything.

Chase easy wins at the top of the cycle (most risk)… and ignore the deep opportunities at the bottom of the cycle (least risk).

Here’s the uncomfortable truth:

It’s not about what you know.

It’s about what you can tolerate.

If you can tolerate the awkwardness of a new conversation… the silence after a first pitch when you thought there would be applause… the discomfort of stepping into the unfamiliar role as a financial educator…

…you can leverage that discomfort and ratchet your business up exponentially.

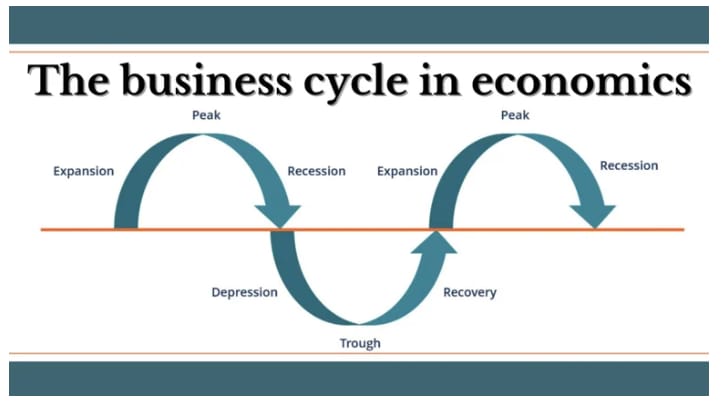

Where are you in your current cycle? Where is the industry?

So Let Me Ask You…

How many financial advisors have you met with in the last 30 days?

Not thought about. Not planned to. Not “intended to.”

Met. With.

Because that number? That’s your future talking.

Your network is your future net worth!

a BORROW SMART CONCEPT

Liquidity is a Liability Driven Concept

if water (liquidity) is rising, what happens to everything (assets)?

Understanding how new money enters our economy is key to grasping the forces behind stock market trends and overall economic health. Contrary to popular belief, new money is predominantly created through borrowing—when banks issue loans, new money is effectively generated. This increases the money supply, adding liquidity to the economy.

Liquidity, simply put, is the ease with which money flows through the economy, and the more of it there is, the easier it flows. High liquidity usually means more spending, borrowing, and investing. When banks extend credit, businesses and individuals gain purchasing power. Businesses invest in growth, hiring, and innovation. Individuals purchase goods and services, driving corporate earnings higher and that drives stocks prices higher. You feel wealthier as your assets grow, so you spend more!

This cycle of liquidity significantly impacts the stock market. With more liquidity available, investors have additional capital to invest in stocks and assets, pushing prices higher. Conversely, tightening liquidity—when borrowing slows or central banks raise interest rates—can lead to a decrease in money supply, potentially stalling economic growth and causing stock prices to decline. Rates have been higher, but with so much liquidity, the market is buoyant to say the least.

Watch liquidity closely to better anticipate economic cycles and market opportunities.

Ultimately, liquidity through borrowing isn't just an economic detail—it's a cornerstone of economic vitality and market dynamics. This is your business; you are providing liquidity through lending, which creates new money.

you can have different parts of the economy in different stages of a cycle

LIABILITIES

What’s Happening?

this is a big form of new liquidity

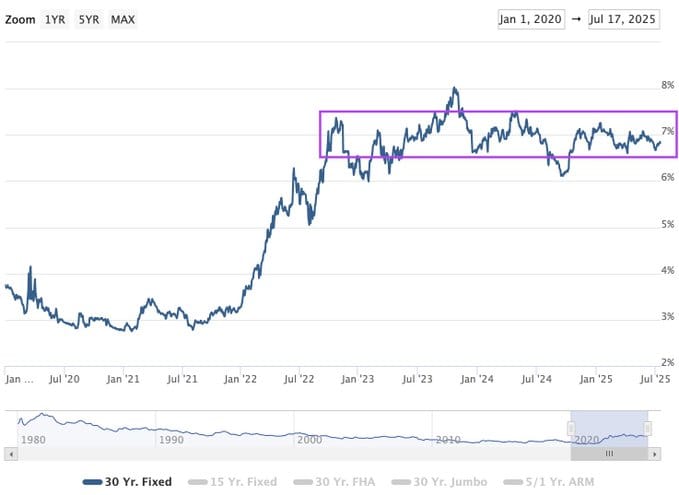

rates staying sideways in the 6.5 - 7.5% range - do they break lower or higher?

the real estate market is hungry for lower rates, lower rates increase liquidity

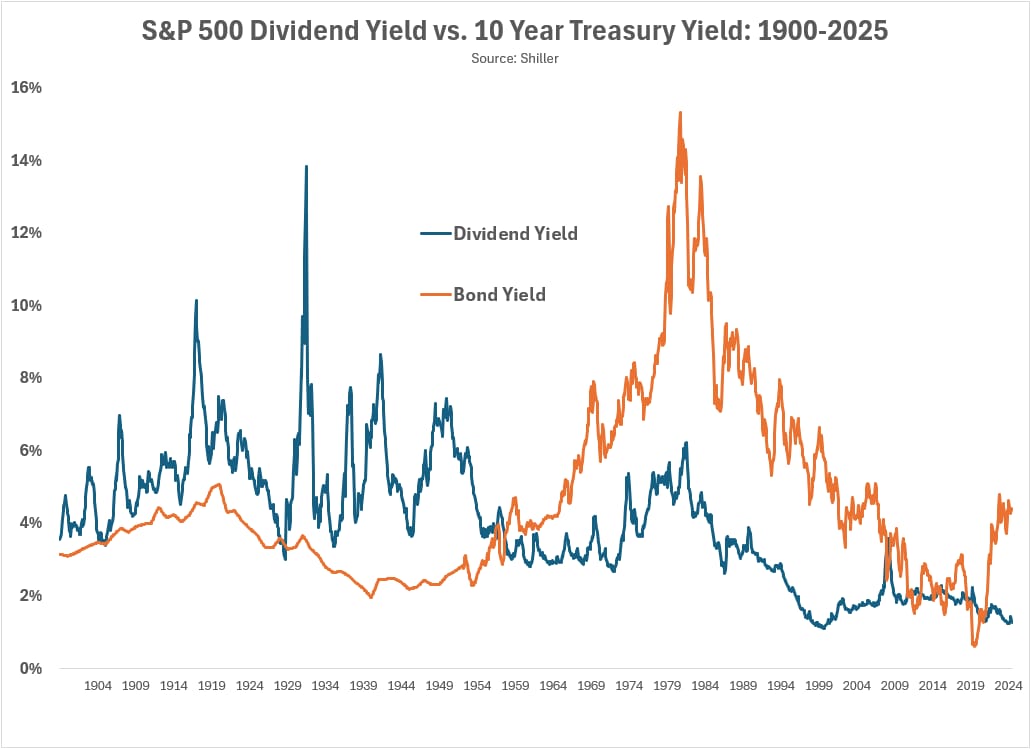

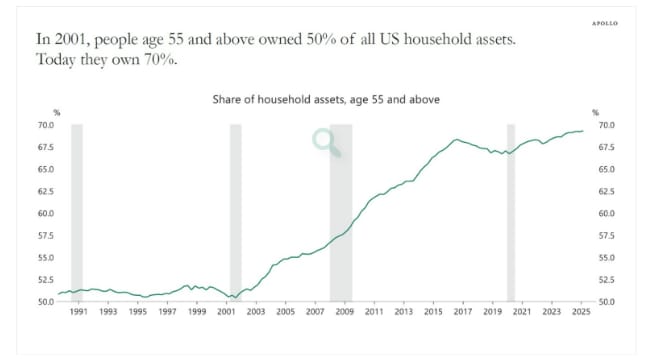

right now seniors are earning a lot more on their bonds than their stocks (yields)

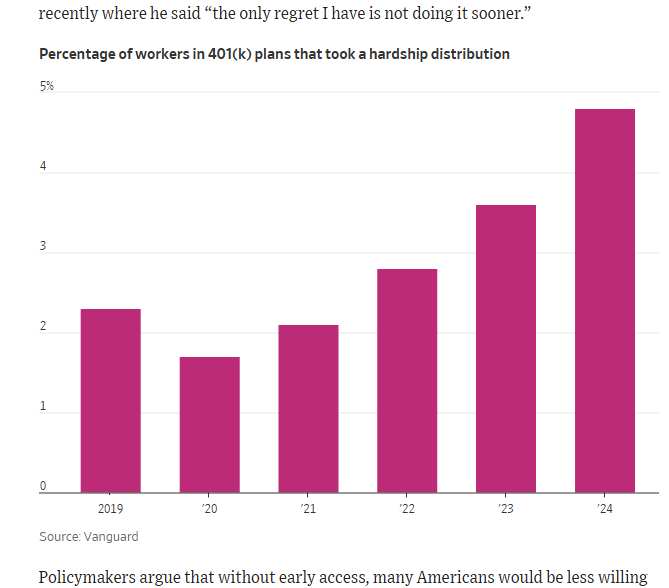

but many are having to borrow to live

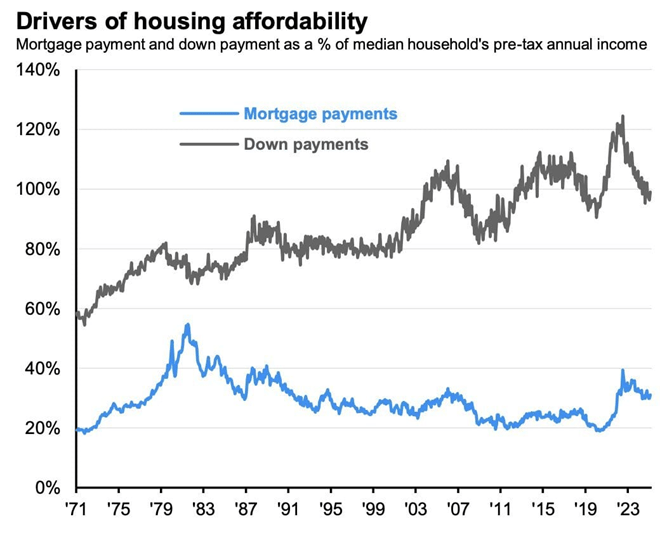

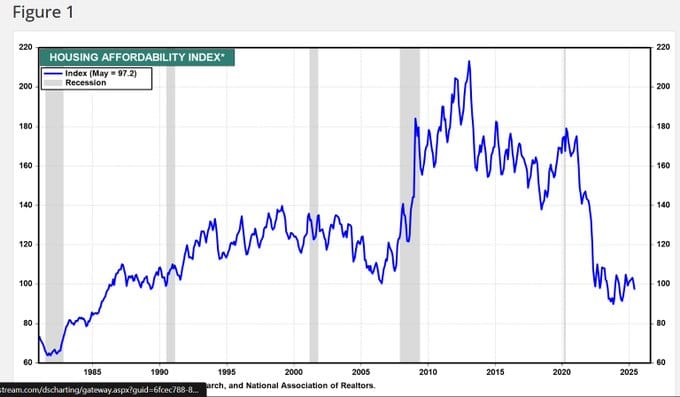

housing affordability …

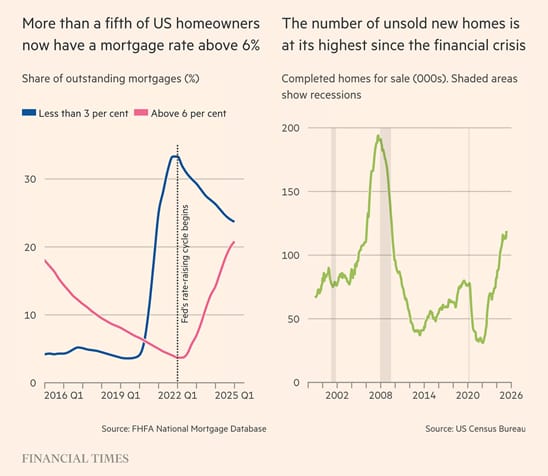

20% are above 6%, prices under pressure

This is the level of focus you want to develop: Credit: Dipin Sreepadmam

REAL ESTATE

What’s Happening?

big investors are back

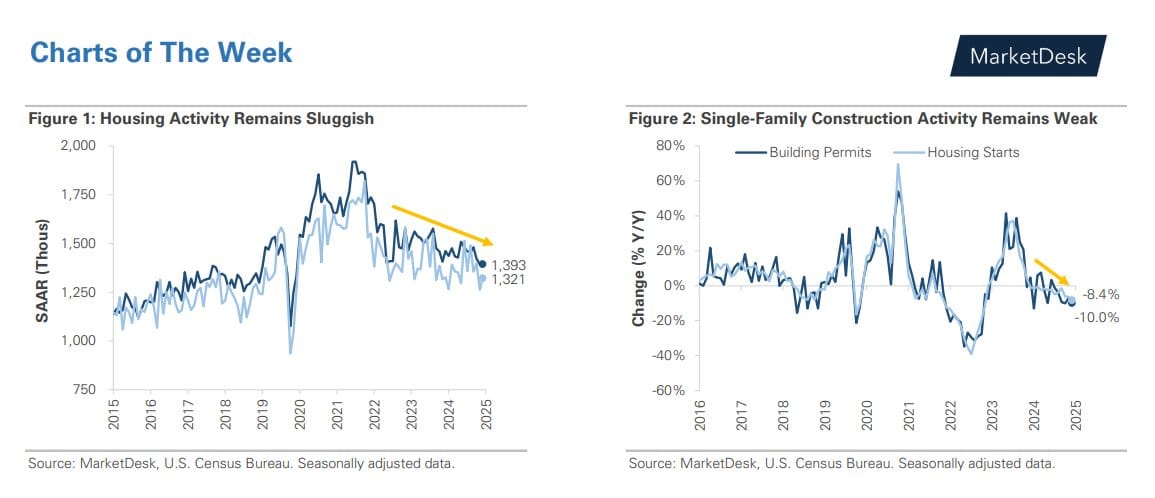

overall housing affordability is actually not as bad as it seems

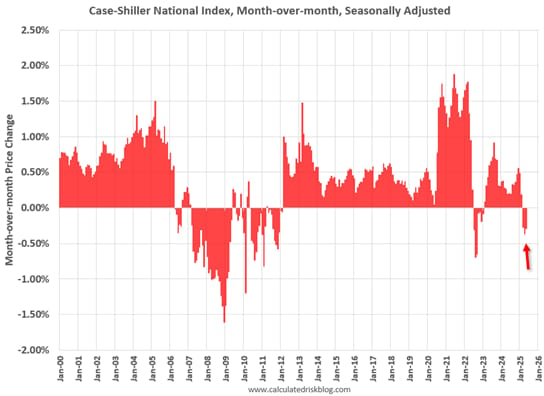

housing prices only up 1% in the last year

and house prices are going down again nationally in more recent data

because inventory is grinding higher, when a house is more liquid (more of them) supply saturates demand, so PRICE is dropped to drive more demand

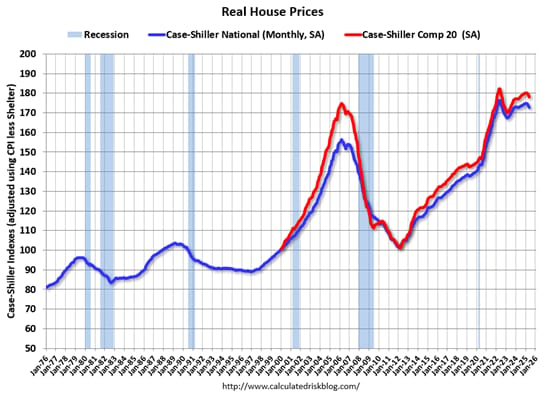

another look from Calculated Risk

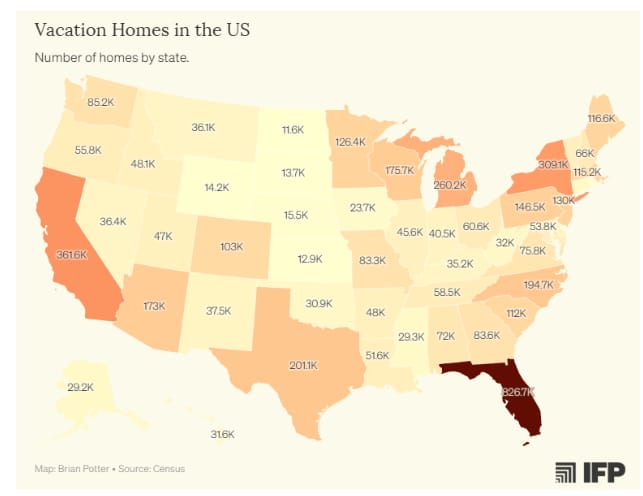

vacation homes are still strong, driven by wealth and foreigners

first time home buyers are not helping

Every moment, some form grows perfect in hand or face; some tone on the hills or the sea is choicer than the rest; some mood of passion or insight or intellectual excitement is irresistibly real and attractive to us—for that moment only. Not the fruit of experience, but experience itself, is the end. A countable number of pulses only is given to us of a variegated, dramatic life. How may we see in them all that is to be seen in them by the finest senses? How shall we pass most swiftly from point to point, and be present always at the focus where the greatest number of vital forces unite in their purest energy? To burn always with this hard, gemlike flame, to maintain this ecstasy, is success in life.

—Walter Pater, Studies in the History of the Renaissance (1873)

ASSETS

What’s Happening?

sea of GREEN!

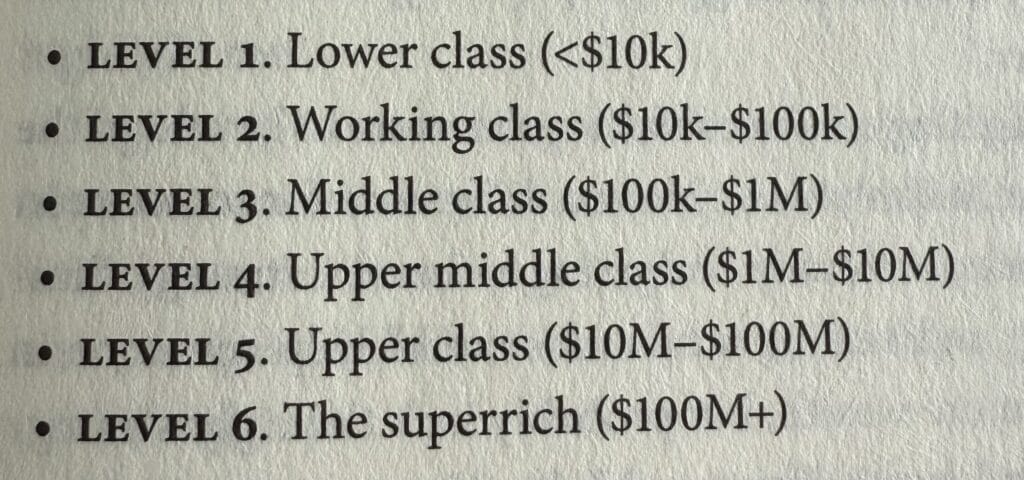

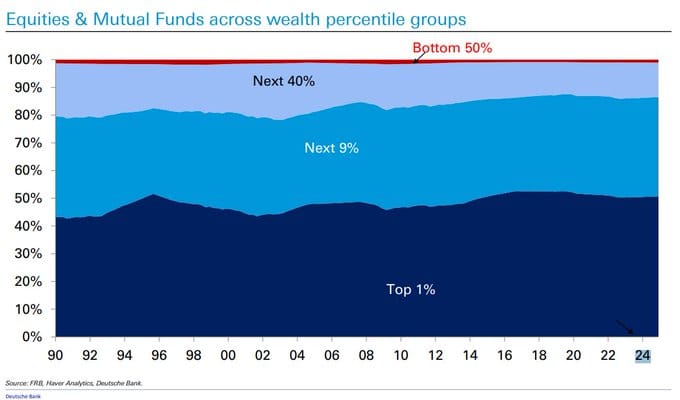

most of the benefits are going to those that already have the savings!

i’ve shared a version of this before, learn to trade a little - this one works well

buy when vix is high, sell when vix is low!

from: A Wealth of Common Sense - the Millionaire Delusion

from Scott Galloway

another look

markets move, within predictable RANGES

ON BEING HUMAN

What’s Worth Sharing?

DOPAMEMES

And Other Happy Moments…

Was this email forwarded to you? Sign up here.

AI

and The Future of Work…

@rachelthecatlovers Just checked the home security cam and… I think we’ve got guest performers out back! @Ring #bunny #ringdoorbell #ring #bunnies #trampoline