- The Borrow Smart Chronicles

- Posts

- Use a 401(k) to Buy a House?

Use a 401(k) to Buy a House?

Let's play around with this changing scenario... proposed by the administration.

Todd Ballenger

January 21, 2026

“Using a 401(k) to buy a home isn’t stealing from your future — it’s trading one form of shelter for another. The real question isn’t can you do it, but whether the house you’re buying will compound better than the dollars you’re unlocking.”

a BORROW SMART CONCEPT

401(k) to a New Castle:

Navigating the New Rules of Home Buying

For decades, touching your 401(k) before age $59.5 was the ultimate financial "no-no." But as housing prices soar, the rules are changing. With new proposals aiming to slash penalties and double the amount you can access, is it finally time to raid the piggy bank for a down payment?

It's an interesting topic, and I've tried to explore it the way I like to explore it, through math and numbers, which you'll get a chance to play around with on my page on this below.

The Old Guard vs. The New Wave

Under the Old Rules, you were caught between a rock and a hard place. You could take a loan (capped at $50,000) and risk a massive tax bill if you changed jobs, or take a "hardship withdrawal" and light $10% of your money on fire in penalties.

The New Proposal flips the script. By proposing penalty-free access to up to $100,000, the goal is to bridge the "affordability gap." Instead of a loan you must repay, it treats your 401(k) as a flexible source of equity.

The "Rules of Thumb" for New Home Buyers

GO If:

Your local home prices are rising faster than your retirement investments would grow

The extra funds get you to a 20% down payment and eliminate PMI

You're buying in a high-cost market and have no other path to homeownership

You have a stable job with a low risk of layoff (for the current loan option)

You're older and have less time for compound growth anyway

NO-GO If:

You're young and have decades for that money to compound

You'd be draining a large percentage of your retirement savings

Your housing market is flat or declining

Your job situation is uncertain

You can qualify for a home without tapping retirement funds

You're not buying a primary residence you'll stay in long-term

The One-Sentence Test

If pulling this money means you'll struggle to retire comfortably, it's a no-go, no matter how appealing the house looks today.

The Bottom Line

The proposed rules make the 401(k) a powerful tool for home ownership, but remember: IT DEPENDS, and knowing what that depends on is the key to most financial questions.

Key Borrow Smart Concept:

You can borrow for a house, but you can't borrow for retirement.

Use the 401(k) as a bridge, not a foundation. If your ‘it depends’ makes sense.

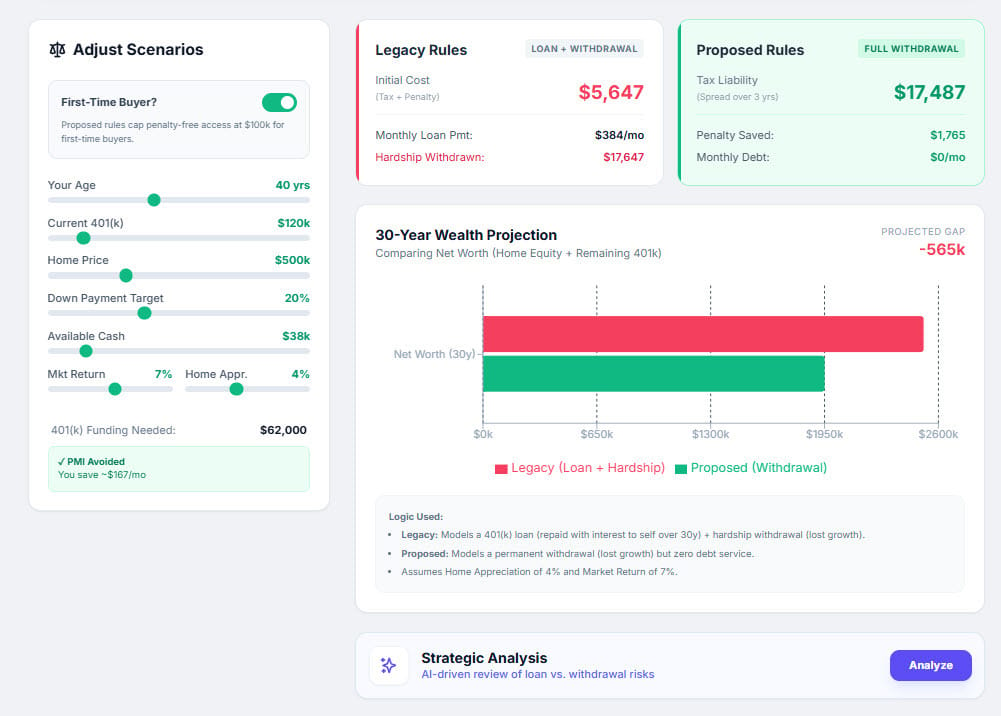

Click the image to view an interactive inquiry on this topic…

It's somewhat new to me, so if you feel like I'm missing something,

feel free to reach out and let me know. [email protected]

Was this email forwarded to you? Sign up here.